How are India’s financial inclusion schemes connecting millions to the mainstream?

Synopsis

Discover how India's financial inclusion schemes are reshaping the nation's economic landscape. From PMJDY to MUDRA, these initiatives are empowering millions, especially women, by integrating them into the formal banking system. Explore the transformative impact of UPI and other policies in promoting financial literacy and reducing reliance on informal finance.

Key Takeaways

Financial inclusion initiatives are reaching millions across India.

Women are significantly represented in programs like PMJDY.

UPI has transformed digital payments , accounting for 85% of transactions.

Financial literacy is crucial for preventing digital fraud.

Credit schemes target marginalized communities to support entrepreneurship.

New Delhi, Aug 11 (NationPress) The government’s financial inclusion initiatives—from Pradhan Mantri Jan Dhan Yojana (PMJDY) to MUDRA and the essential UPI-based digital payments—are transforming India’s narrative from a metropolitan focus to a truly national perspective, according to a recent report.

As stated by Prime Minister Narendra Modi, “Economic progress should not be confined to a select few cities and citizens. Development must encompass everyone and every region.”

“In reality, this inclusiveness is not just talk; it’s been propelled by carefully integrating policy, technology, and community outreach into a remarkable network of accessibility,” the report in India Narrative reveals.

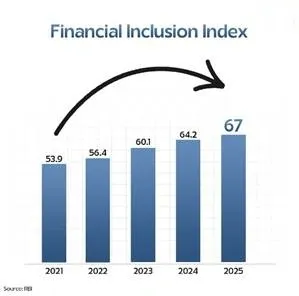

The Financial Inclusion Index, launched in 2021, is based on 97 indicators covering banking, insurance, pensions, investments, and postal services.

Its three sub-indices—Access, Usage, and Quality—evaluate not only the infrastructure's reach but also whether individuals actively utilize and comprehend financial products.

“The scale of implementation has been astonishing. The Pradhan Mantri Jan Dhan Yojana (PMJDY) alone has integrated 55.98 crore (560 million) people into the formal banking system, with over half being women. A network of 13.55 lakh (1.35 million) ‘Bank Mitras’—local banking representatives—now delivers services to remote villages,” the report notes.

Women predominantly hold Jan Dhan accounts, and the Atal Pension Yojana now features 48 percent female subscribers.

Furthermore, UPI accounts for 85 percent of all digital transactions in India and nearly half of global real-time digital payments.

Daily UPI transactions have surpassed 700 million for the first time, reaching 707 million as per the latest data from the National Payments Corporation of India (NPCI). This milestone was achieved on August 2. The number of daily transactions has doubled over the past two years, despite a slowdown in growth compared to earlier years.

However, as rural households increasingly adopt mobile banking, they also face a heightened risk of digital fraud. In response, the emphasis on financial education is shifting towards fraud prevention and grievance resolution.

Credit programs like MUDRA and Stand Up India specifically target SC, ST, and women entrepreneurs.

“The Mahila Sammriddhi Yojana equips women with craft skills and organizes them into self-help groups with access to credit. The Kisan Credit Card, now aiding over 7.7 crore farmers, minimizes reliance on informal moneylenders and enhances agricultural productivity,” the report states.

The World Bank’s Global Findex 2025 now indicates that account ownership in India stands at 89 percent—a significant increase from 35 percent in 2011.

Point of View

It’s crucial to highlight the positive strides India is making towards financial inclusion. The government's initiatives are not just policies but lifelines for millions, especially women and marginalized communities. By focusing on technology and outreach, these programs aim to create an equitable financial environment, fostering growth and stability for all citizens.

NationPress

6 Jul 2026

Frequently Asked Questions

What is the Pradhan Mantri Jan Dhan Yojana?

The Pradhan Mantri Jan Dhan Yojana is a government initiative aimed at ensuring access to financial services such as banking, insurance, and pensions for all, especially the underprivileged.

How has UPI impacted digital transactions in India?

UPI has revolutionized digital transactions in India, accounting for 85% of all transactions, and has played a crucial role in enhancing financial inclusion.

What measures are in place to combat digital fraud?

The government is focusing on financial literacy, particularly on fraud prevention and grievance redressal, to protect users in the growing mobile banking ecosystem.

What is the significance of the Financial Inclusion Index?

The Financial Inclusion Index measures access, usage, and quality of financial services, providing insights into how well financial products are serving the population.

How do programs like MUDRA support entrepreneurs?

Programs like MUDRA and Stand Up India provide credit and training specifically targeting SC, ST, and women entrepreneurs, enabling them to thrive in their ventures.