How has the Pradhan Mantri Jan Dhan Yojana Transformed Financial Inclusion in India?

Synopsis

Discover how the Pradhan Mantri Jan Dhan Yojana has revolutionized financial inclusion in India, impacting millions and transforming the banking landscape. This 11-year journey highlights empowerment, digital success, and global recognition.

Key Takeaways

PMJDY has opened over 55.90 crore Jan Dhan accounts, empowering millions.

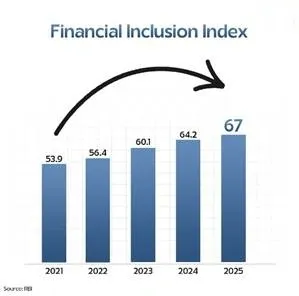

67% of these accounts are in rural areas, enhancing access to banking.

The initiative has significantly increased women's participation in the financial system.

Digital financial services have expanded dramatically under PMJDY.

PMJDY is a vital component of India’s economic growth and inclusion strategy.

New Delhi, Aug 1 (NationPress) Today, it’s commonplace for individuals in India to possess a bank account. However, prior to a decade ago, nearly half of the country's households faced barriers to banking services, even after 65 years of independence.

Many of the economically disadvantaged and marginalized groups, particularly in rural regions, were excluded from the official banking framework. They had no option but to risk their savings at home and rely on predatory lenders demanding exorbitant interest rates. This lack of financial security left them with no hope for a better future.

As a former Prime Minister pointed out, out of every 100 paise intended for the impoverished, only 15 paise reached the actual beneficiaries, while the remaining 85 paise was consumed by intermediaries.

A Game Changer

In this backdrop, the introduction of Pradhan Mantri Jan Dhan Yojana (PMJDY) in 2014, under the guidance of Prime Minister Narendra Modi, has been a revolutionary step towards enhancing financial inclusion.

As this initiative marks its 11th anniversary on August 28, 2025, it is evident that it has brought dignity to millions of individuals, significantly benefiting women, youth, and marginalized communities by integrating them into the economic framework of the nation.

Financial Inclusion

By establishing the groundwork for people-centric economic initiatives such as direct benefit transfers, PM-KISAN, and improved wages under MGNREGA, along with life and health insurance coverage via bank accounts, PMJDY stands out as one of the most significant financial inclusion efforts globally.

The success of PMJDY is evident from the staggering growth of Jan Dhan Accounts, which soared to over 55.90 crore from just 14.72 crore in March 2015. Approximately 67 percent of these accounts were opened in rural or semi-urban regions.

With Jan Dhan accounts fostering savings and promoting digital financial habits, these accounts have amassed a deposit balance exceeding Rs 2.63 lakh crore, a significant leap from Rs 15,670 crore in March 2015.

Empowerment of Weaker Sections

With features such as zero balance accounts, complimentary RuPay Cards, and accidental insurance of Rs 2 lakhs for account holders, along with an overdraft facility of Rs 10,000 for eligible individuals, PMJDY has empowered low-income and marginalized groups over the past 11 years.

Notably, the Atal Pension Yojana (APY) has experienced a surge in enrolments, reaching 7.33 crore by January 2025. The Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY) has enrolled 22.52 crore individuals, disbursing Rs 17,600 crore for 8.8 lakh claims, while the Pradhan Mantri Suraksha Bima Yojana (PMSBY) has covered 49.12 crore people, processing Rs 2,994.75 crore for accident claims.

Eliminating Middlemen

Jan Dhan has also become a crucial component of the JAM Trinity (Jan Dhan, Aadhaar, and Mobile), aiming to eradicate the influence of middlemen and touts who have profited from public exploitation through Direct Benefit Transfers (DBT).

Jan Dhan accounts are utilized for DBT in 321 government schemes, a significant increase from just 28 in 2013-14, including Ayushman Bharat, PM-Kisan for farmers, PM SVANidhi for street vendors, and more.

The total funds transferred have escalated from approximately Rs 7,400 crores in 2013-14 to nearly Rs 25 lakh crores, contributing to an estimated savings of around Rs 4.31 lakh crore for the government and assisting about 25 crore individuals in overcoming multidimensional poverty in the last nine years.

Facilitating Access to Credit

The Jan Dhan Yojana has liberated the economically disadvantaged from the grip of usurious lenders, enabling account holders to access loans from banks and financial institutions. For example, loan approvals under the Mudra scheme increased at a compounded annual growth rate of 9.8 percent from 2018-19 to 2023-24, empowering individuals to elevate their incomes through formal lending.

Women Empowerment

PMJDY has emerged as a formidable instrument for empowering women, particularly those in the informal sector lacking access to formal old-age income security schemes. Their financial instability was further compounded by irregular incomes and limited social security access.

PMJDY has included women into the fold of financial inclusion, with over 30.37 crore (55.7 percent) of total Jan Dhan accounts belonging to them. By ensuring equal opportunities in the formal financial space, PMJDY has facilitated women's access to various social security and credit-linked initiatives.

As of November 2023, out of the 44.46 crore loans sanctioned under the Pradhan Mantri Mudra Yojana (PMMY), 30.64 crore (69 percent) were allocated to women, with the average credit amount rising from Rs 39,000 in 2015-16 to Rs 1 lakh in 2023-24. As of January 27, 2025, the Stand-Up India Scheme has aided 1,94,804 women entrepreneurs, with banks approving Rs 62,426.52 crore to promote entrepreneurship among women and SCs & STs.

Digital Success

PMJDY has enabled the issuance of over 38 crore complimentary RuPay cards and the installation of 79.61 lakh PoS/mPoS machines. The advent of mobile payment systems like UPI has elevated India's digital banking services, with UPI transactions through RuPay cards soaring from Rs 92 crore in FY 2017-18 to Rs 8,371 crore in FY 2022-23.

Likewise, the total number of RuPay card transactions at PoS and E-commerce outlets has expanded from Rs 28.28 crore in FY 2016-17 to Rs 126 crore in FY 2022-23.

Today, India stands as a global frontrunner in real-time payments, accounting for 48.5 percent of the total volume, with PMJDY playing a pivotal role in integrating millions of previously unbanked individuals into the formal banking system.

Global Recognition

PMJDY has garnered international acclaim for its contribution to financial inclusion. According to the World Bank’s Global Findex 2025 report, India has achieved nearly universal financial account ownership, with 89 percent of adults now holding an account, compared to just 35 percent in 2011.

A G20 report by the World Bank highlighted that India accomplished its financial inclusion targets in a mere 6 years, which would have otherwise taken 47 years. India even set a Guinness World Record by opening over 1.80 crore bank accounts during the Financial Inclusion Campaign under Jan Dhan Yojana, surpassing China in financial inclusion metrics, as per the SBI report of 2021.

Suggestions

Awareness Campaign: Launch an awareness initiative in rural and semi-urban areas to inform the adult population about the advantages of bank accounts.

Expansion of Bank Network: Increase the number of bank branches in rural and semi-urban areas to enhance access to banking services.

Strengthening Cooperative Banks: Modernize and enhance cooperative banks to adopt financial technology that meets the credit demands of rural India.

Financial Literacy: Implement digital and financial literacy programs to empower beneficiaries to fully utilize the benefits of the Jan Dhan Yojana.

Special Financial Product Design: Create innovative financial products for PMJDY account holders to deepen financial inclusion.

By empowering millions, particularly from marginalized communities, PMJDY has established a solid foundation for inclusive economic growth towards a Viksit Bharat by 2047. Every citizen should now actively contribute to India’s economic prosperity.

(The author is Pro Chancellor, Chandigarh University and can be contacted at himani.sood@cumail.in)

Point of View

Empowering marginalized communities and ensuring that every citizen has a stake in the nation's economic progress. This initiative reflects a commitment to not only enhancing individual livelihoods but also fostering a more equitable society.

NationPress

9 Aug 2026

Frequently Asked Questions

What is Pradhan Mantri Jan Dhan Yojana?

Pradhan Mantri Jan Dhan Yojana (PMJDY) is a financial inclusion initiative launched by the Government of India in 2014. It aims to provide universal access to banking facilities, including savings and deposit accounts, remittance services, credit, insurance, and pension to the underprivileged sections of society.

How has PMJDY impacted financial inclusion in India?

PMJDY has played a crucial role in increasing bank account ownership in India, with over 55.90 crore Jan Dhan accounts opened since its inception. This initiative has empowered millions by providing access to financial services that were previously unavailable to them.

What benefits do Jan Dhan account holders receive?

Jan Dhan account holders enjoy various benefits, including zero balance accounts, free RuPay cards, accidental insurance, and eligibility for loans and credit facilities. These benefits help enhance the financial security and well-being of account holders.

How has PMJDY contributed to women's empowerment?

PMJDY has significantly empowered women by ensuring their inclusion in the formal financial system. Over 30.37 crore (55.7 percent) of Jan Dhan accounts are held by women, providing them access to credit and social security schemes that enhance their financial independence.

What is the future of financial inclusion in India?

The future of financial inclusion in India looks promising with continued efforts from the government to expand banking services, enhance digital literacy, and develop innovative financial products tailored for the needs of the underprivileged.