Trump signs executive order expanding IRA access for low-income Americans

Synopsis

Trump's new executive order doesn't just tweak retirement policy — it targets a structural blind spot in the US savings system. By offering up to $1,000 in annual matching funds to workers earning under $35,000 and allowing charitable contributions into IRAs, the administration is moving without waiting for Congress — while openly acknowledging it will need Congress to go further.

Key Takeaways

President Donald Trump signed an executive order on 1 May expanding retirement savings access for millions of Americans.

Low-income workers with incomes below $35,000 could receive up to $1,000 per year in government matching funds deposited into their accounts.

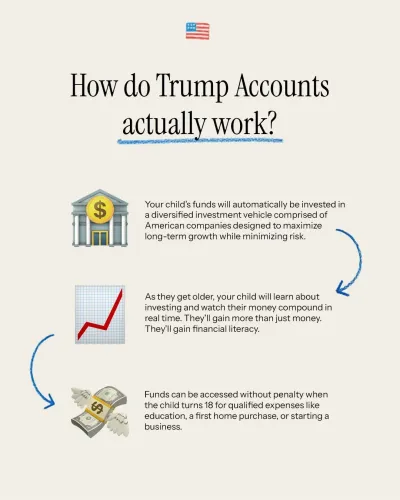

The programme, dubbed TrumpIRA , also allows charitable organisations to contribute to individuals' retirement accounts.

National Economic Council Director Kevin Hassett confirmed discussions are underway to extend benefits to middle-income Americans .

Trump acknowledged that broader expansion beyond the executive order will require Congressional approval and called for a bipartisan effort.

US President Donald Trump on 1 May signed an executive order aimed at expanding access to retirement savings accounts for millions of Americans, particularly low-income workers and those without employer-sponsored plans. The initiative, which Trump described as a "historic executive order," is designed to give workers outside traditional employment structures access to retirement accounts modelled on those available to federal employees.

What the Executive Order Does

At the core of the order is a government-matching mechanism: according to Trump, low-income Americans could receive up to $1,000 per year in matching funds deposited directly into their retirement accounts. National Economic Council Director Kevin Hassett clarified that the match targets individuals with incomes below $35,000, addressing what he described as a structural gap in the retirement savings system.

The programme will also permit charitable contributions into individual retirement accounts, broadening participation beyond government matching alone. Hassett noted, "We've also made it clear that in the TrumpIRA charities can contribute to other people's accounts as well."

The Long-Term Projection

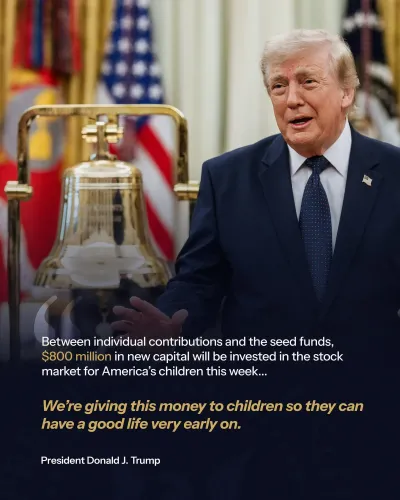

Trump illustrated the potential impact with a specific projection. "If a 25 year old… invests just $165 a month… they will have an estimated $465,000 in their account by the time they're 65 years old," he said, adding, "In other words, they'll be rich." The administration framed the initiative as transformative for gig workers, freelancers, and informal-sector employees who have historically been underserved by employer-based retirement structures.

What the Government Said

Speaking at the signing, Trump said: "This afternoon, I'm thrilled to sign a historic executive order expanding access to high-quality retirement savings accounts for millions of Americans." He added that for workers without employer-sponsored plans, "this will be really revolutionary because they'll be covered."

Hassett confirmed that the administration is already in discussions to widen eligibility. "We're working with Congress to significantly expand this program," he said, noting that talks include extending benefits to middle-income Americans. Trump, however, acknowledged that broader expansion would require legislative approval. "To take it to the next level, we need Congressional approval… it should be bipartisan," he said.

Background and What Comes Next

The US retirement system has long depended heavily on employer-based plans, leaving gig workers and informal labour segments with limited options. Efforts to close this coverage gap have attracted bipartisan attention in recent years, though legislative action has been slow. This executive order represents the administration's attempt to act within existing executive authority while building momentum for a broader Congressional push. Discussions on expanding eligibility to middle-income earners are reportedly already underway on Capitol Hill.

Point of View

A posture that sets up a ready-made campaign contrast. But the structural problem is real: America's retirement coverage gap disproportionately affects gig workers and the informal economy, groups that have grown significantly since the 401(k) system was designed. The $1,000 match is modest against the scale of the shortfall, and the charitable contribution provision, while novel, raises questions about who benefits and how contributions will be regulated. The real test is whether the bipartisan Congressional push materialises — or whether this remains an executive-order-sized solution to a legislative-sized problem.

NationPress

5 Aug 2026

Frequently Asked Questions

What is the TrumpIRA executive order?

It is an executive order signed by President Donald Trump on 1 May 2025, creating expanded retirement savings accounts — referred to as TrumpIRA — for millions of Americans who lack employer-sponsored plans. The order includes government matching funds of up to $1,000 per year for low-income workers earning below $35,000.

Who is eligible for the matching funds under the TrumpIRA?

The matching funds are currently targeted at low-income Americans with incomes below $35,000, according to National Economic Council Director Kevin Hassett. The administration is working with Congress to potentially expand eligibility to middle-income Americans as well.

Can charities contribute to someone's TrumpIRA account?

Yes. The executive order explicitly allows charitable organisations to contribute to other individuals' retirement accounts under the TrumpIRA framework, broadening participation beyond government matching alone.

Will the programme expand beyond low-income workers?

Broader expansion to middle-income Americans would require Congressional approval, which Trump has publicly acknowledged. The administration says discussions with Congress are already underway and has called for the effort to be bipartisan.

Why does the US retirement coverage gap exist?

The US retirement system has historically relied on employer-based plans such as 401(k)s, leaving gig workers, freelancers, and informal-sector employees without access to structured savings vehicles. This structural gap has grown as non-traditional employment has expanded over recent decades.