UPI cited by US lawmakers as model for payments reform debate

Synopsis

India's UPI has crossed the Pacific — not as a product, but as a policy argument. At a US Congressional hearing, Stripe's Vice Chair and Congresswoman Rashida Tlaib both invoked UPI's scale to push for a federal payments charter that would let fintechs bypass traditional banking rails. It is a rare moment when an Indian public infrastructure model shapes a Washington debate.

Key Takeaways

The House Financial Services Committee's Subcommittee on Financial Institutions held a hearing on Wednesday, 25 June on modernising US payment infrastructure .

Stripe Vice Chair Eileen O'Mara cited India's UPI and Brazil as evidence that open payment rails drive innovation at scale.

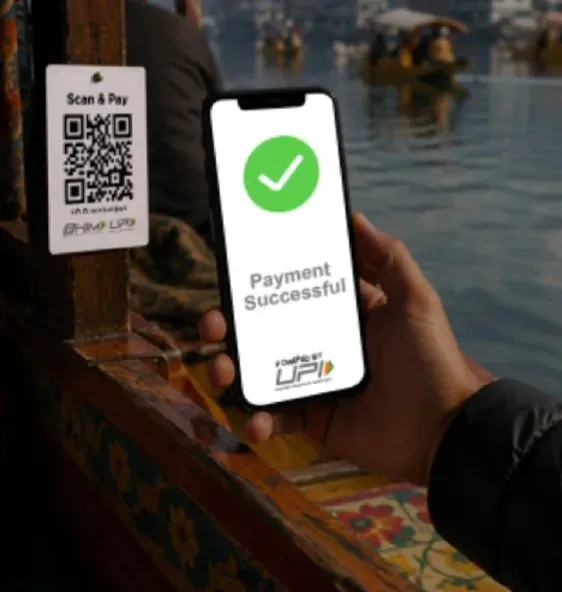

Congresswoman Rashida Tlaib noted that UPI , operated by the National Payments Corporation of India , processes billions of transactions monthly.

Lawmakers debated a dedicated federal payments charter to give regulated fintechs direct access to Federal Reserve payment rails.

The National Community Reinvestment Coalition urged strong consumer protections for any non-bank entity gaining payment system access.

US lawmakers examining the future of America's payment infrastructure held up India's Unified Payments Interface (UPI) as a benchmark for how open, publicly backed payment rails can catalyse private-sector innovation. The discussion unfolded on Wednesday during a hearing of the House Financial Services Committee's Subcommittee on Financial Institutions in Washington, where fintech companies pressed Congress to modernise regulations governing non-bank access to Federal Reserve payment systems.

What the Hearing Was About

At the centre of the debate was whether the United States should create a dedicated federal payments charter — one that would allow regulated fintech firms to tap Federal Reserve payment rails directly, bypassing the current reliance on traditional banking intermediaries and a fragmented web of state licences. Lawmakers from both parties acknowledged the urgency of faster, cheaper payments as digital commerce expands, though they differed on how broadly access should be extended.

What Stripe's Vice Chair Said

Eileen O'Mara, Vice Chair at Stripe, told the subcommittee that countries that have opened their payment infrastructure to competition have generated measurable innovation. She cited Brazil and India as leading examples. 'The UK did it in 2017, the EU in 24, and the results are real,' she said, adding: 'We saw the very same thing happen with UPI in India on an even larger scale.'

O'Mara argued that while the United States already operates the FedNow instant payment system, it 'lacks a product layer on top — exactly what payment companies like Stripe would build, with the direct access that could drive significant adoption.' She also pushed back against a binary regulatory framework, saying the existing rules were built around whether a company is 'a bank or you're not a bank,' while payment processors operate a fundamentally different model. 'We do not take deposits, and we do not lend,' she said. 'What we're advocating for is that we are regulated for the business and activity that we do, which is payment processing.'

India's UPI in the Spotlight

Congresswoman Rashida Tlaib specifically highlighted India's digital payments success, noting that UPI — operated by the National Payments Corporation of India (NPCI) — processes billions of transactions each month. She contrasted this with the US system, arguing that the achievements of India and Brazil demonstrated that 'large-scale payment systems offering free instant transactions' are already a functioning reality for hundreds of millions of users. This is not the first time UPI has been invoked in Western policy circles; the system has increasingly become a reference point in global fintech reform discussions.

Consumer Protection Concerns

Tara Flynn of the National Community Reinvestment Coalition urged lawmakers to ensure that any non-bank entity gaining access to payment infrastructure be subject to robust consumer protections, community investment obligations, and rigorous regulatory oversight. Her intervention signalled that the push for openness faces a significant counterweight from advocacy groups concerned about weakening the safeguards embedded in the traditional banking system.

What Comes Next

The hearing reflects a pivotal moment in Washington's fintech policy debate. A federal payments charter, if enacted, would fundamentally reshape how companies like Stripe operate in the United States — and could accelerate the kind of adoption curves that India's UPI demonstrated after its 2016 launch. No legislative timeline has been confirmed, but the bipartisan acknowledgement of the problem suggests the issue will remain on Congress's agenda in the months ahead.

Point of View

Not the other way around. But the comparison has limits. UPI succeeded in part because of a specific Indian context — demonetisation, a large unbanked population, and government-mandated interoperability. The US fintech lobby is selectively borrowing the UPI narrative to argue for deregulation, while consumer advocates rightly flag that India's model also came with public-interest guardrails. Congress should examine the full picture, not just the adoption curve.

NationPress

9 Aug 2026

Frequently Asked Questions

Why did US lawmakers mention India's UPI in a Congressional hearing?

US lawmakers cited India's UPI as a real-world example of how open, publicly backed payment infrastructure can drive large-scale private-sector innovation. The reference came during a House Financial Services subcommittee hearing on whether the US should allow non-bank fintechs direct access to Federal Reserve payment rails.

What is the federal payments charter being debated in the US?

A federal payments charter would create a dedicated regulatory category for fintech payment companies, allowing them to access Federal Reserve payment infrastructure directly rather than operating through traditional banks or a patchwork of state licences. Companies like Stripe have argued this would accelerate adoption of instant payments in the US.

What did Stripe's Eileen O'Mara say about UPI at the hearing?

Eileen O'Mara, Vice Chair at Stripe, said that countries opening payment infrastructure to competition have seen significant innovation, citing UPI in India as an example that happened 'on an even larger scale.' She argued the US FedNow system lacks the product layer that direct-access fintechs could build.

Who operates UPI in India and how large is it?

UPI is operated by the National Payments Corporation of India (NPCI) and processes billions of transactions each month. Congresswoman Rashida Tlaib cited it as proof that large-scale, free instant payment systems are already a functioning reality globally.

What consumer protection concerns were raised at the hearing?

Tara Flynn of the National Community Reinvestment Coalition urged that any non-bank entity gaining access to payment systems be subject to strong consumer protections, community investment obligations, and rigorous regulatory supervision, cautioning against weakening safeguards built into the traditional banking system.