Is India on the Path to Becoming the 3rd Largest Economy While Pakistan Faces Collapse?

Synopsis

The contrasting economic trajectories of India and Pakistan starkly illustrate their divergent paths since independence, with India progressing rapidly towards becoming the world's third-largest economy while Pakistan faces severe economic challenges. This article explores the implications of these developments.

Key Takeaways

India's GDP is projected to reach $3.88 trillion in 2024.

Pakistan's economy is struggling with only $0.37 trillion.

India is on track to become the fourth-largest economy by 2025.

Pakistan faces significant risks due to political instability.

Moody's rates India's economic outlook as stable.

New Delhi, May 7 (NationPress) As Pakistan threatens to retaliate against India's actions targeting terrorist infrastructure within its borders, the glaring economic disparity between these two neighboring nations highlights the vastly different trajectories they have followed since gaining independence from British colonial rule.

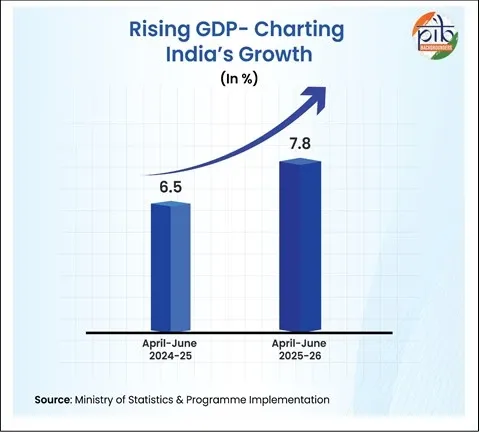

India has emerged as the globe's fastest-growing economy, with the World Bank projecting the country's GDP to reach approximately $3.88 trillion in 2024, dwarfing Pakistan's economy at a mere $0.37 trillion.

By 2025, India is set to ascend to the status of the world's fourth-largest economy, as its nominal GDP is expected to grow to $4.187 billion, surpassing Japan, according to the IMF's World Economic Outlook report. Furthermore, India boasts a robust foreign exchange reserve of $688 billion.

In contrast, Pakistan teeters on the brink of economic disaster, relying heavily on IMF loans, with its foreign exchange reserves dwindling to just $15 billion.

Interestingly, in the early years following independence, Pakistan's economic growth mirrored India's, supported by U.S. aid and contributions from wealthy Islamic nations.

However, while democratic India concentrated on fostering economic growth and alleviating poverty, Pakistan has endured a series of violent coups and military regimes, with military leaders still exerting influence and promoting antagonism towards its more affluent neighbor. The financing and training of terrorism by Pakistan is a crucial aspect of this ongoing conflict.

Currently, Pakistan faces an economic crisis, exacerbated by political instability and the long-term repercussions of its support for terrorism, resulting in violent conflicts in Balochistan and the North West Frontier Province.

In 2023, Pakistan teetered on the edge of sovereign default and required a $3 billion bailout from the IMF. The nation remains critically reliant on this financial support and is urgently seeking an additional $1.3 billion climate resilience loan.

Meanwhile, global ratings agency Moody's stated on Monday that it assesses India's macroeconomic conditions as stable, even amidst increasing tensions with Pakistan following the tragic terror attack in Pahalgam that claimed the lives of 26 tourists.

However, sustained escalations in tensions with India could adversely impact Pakistan's economy and hinder its ongoing fiscal recovery efforts, according to the Moody's report.

The report further indicated that amidst rising geopolitical tensions, any flare-ups could disrupt access to external financing and place additional strain on Pakistan's foreign exchange reserves, which currently stand at just over $15 billion, far below the amount necessary to meet upcoming external debt obligations.

Moody's noted that the macroeconomic conditions in India remain stable, supported by robust public investment and resilient private consumption, despite potential increases in defense spending that may slow fiscal recovery.

According to the report, India's macroeconomic prospects are bolstered by strong public investment and healthy private consumption, even in the face of heightened tensions. “In a scenario of sustained escalation in localized tensions, we do not foresee major disruptions to India’s economic activity as it maintains minimal economic ties with Pakistan (less than 0.5 percent of India's total exports in 2024).”

Point of View

It's essential to recognize the complex interplay between economic growth and geopolitical tensions. While India continues to build a robust economy, Pakistan's struggles serve as a stark reminder of the consequences of political instability and mismanagement. A balanced approach to reporting is crucial, highlighting both the successes and challenges faced by these neighboring nations.

NationPress

7 Aug 2026

Frequently Asked Questions

What is the current GDP of India and Pakistan?

India's GDP is approximately $3.88 trillion, while Pakistan's GDP is around $0.37 trillion.

Why is Pakistan's economy struggling?

Pakistan is grappling with political chaos, reliance on IMF loans, and the long-term consequences of supporting terrorism.

How is India's economy performing?

India is projected to become the world's fourth-largest economy by 2025, with strong public investment and private consumption.

What impact do tensions with India have on Pakistan's economy?

Increased tensions could hinder Pakistan's fiscal recovery efforts and strain its foreign exchange reserves.

What does Moody's say about India's economic outlook?

Moody's assesses India's macroeconomic conditions as stable, despite potential defense spending increases.