Nepal's Trade Deficit with China Widens: Key Facts

Synopsis

Nepal's imports from China surpassed Rs 195 billion in just the first half of FY2025-26, while exports remain negligible. With BRI contracts overwhelmingly awarded to Chinese firms and Nepal's own central bank flagging structural risk, Kathmandu is caught in a self-reinforcing economic trap that its domestic capital cannot break.

Key Takeaways

Nepal's imports from China surpassed Rs 195 billion in just the first half of financial year 2025-26 , while exports to China remained negligible.

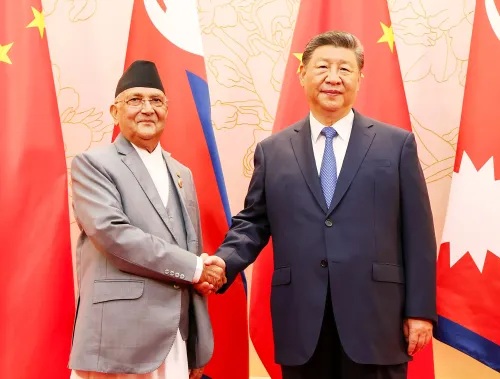

Nepal formally joined China's Belt and Road Initiative (BRI) in 2017 , but over 60 per cent of BRI project contracts globally are awarded to Chinese firms , per World Bank data.

Nepal's industrial output is concentrated in food processing, textiles, and construction materials — sectors directly eroded by cheaper Chinese imports.

Both Nepal's central bank and Finance Ministry have officially flagged import dependence on China as a structural economic risk .

The circular dependency trap means the most available capital to diversify Nepal's economy or build domestic industry is Chinese capital itself — reinforcing the same imbalance.

Nepal's situation reflects a broader regional pattern, with Sri Lanka and Pakistan also experiencing debt and trade asymmetries linked to Chinese economic engagement.

Nepal is grappling with a rapidly deepening trade deficit with China, as import volumes continue to dwarf the country's exports to its northern neighbour. In the first half of financial year 2025-26, Nepal's imports from China crossed Rs 195 billion — spanning electronics, machinery, vehicles, and textiles — while exports to China remained a negligible fraction of that figure, according to a detailed analysis published by Eurasia Review.

The Scale of Nepal's Trade Imbalance

The asymmetry in Nepal-China trade is not a recent phenomenon, but data from the current fiscal year underscores how structurally entrenched the gap has become. Nepal's manufacturing base remains too narrow and undercapitalised to compete meaningfully with Chinese goods flooding its domestic markets.

Sectors such as food processing, textiles, and construction materials — which form the core of Nepal's industrial output — directly overlap with high-volume Chinese import categories. As a result, Nepali producers have experienced consistent erosion of domestic market share, a trend that analysts attribute to both competitiveness gaps and policy failures around foreign direct investment (FDI) terms.

Belt and Road Initiative Deepens Structural Risks

Nepal formally joined China's Belt and Road Initiative (BRI) in 2017, with expectations of large-scale infrastructure financing that would modernise the landlocked nation's connectivity. However, the reality on the ground reflects a pattern seen across BRI recipient countries globally.

According to World Bank research, more than 60 per cent of Chinese-funded BRI projects worldwide are awarded to Chinese firms, compared to approximately 30 per cent in projects financed by non-Chinese institutions. In Nepal's case, domestic construction firms are largely confined to peripheral roles, while Chinese companies capture the more lucrative equipment supply and specialised engineering contracts.

This arrangement effectively recycles Chinese capital back into the Chinese economy, limiting the technology transfer and employment multiplier effects that Nepal's policymakers had anticipated when signing onto the BRI framework.

Policy Warnings from Nepal's Own Institutions

The severity of the situation has prompted formal acknowledgement from Nepal's own financial authorities. Both Nepal's central bank and the Finance Ministry have flagged import dependence on China as a structural risk in their official planning documents — a rare instance of institutional candour about a geopolitically sensitive economic relationship.

The remedies identified are straightforward in theory but extraordinarily difficult in practice. Nepal must either diversify its import sources — which demands new trade agreements and supply chain development — or build domestic productive capacity in import-competing sectors, which requires capital investment and skills development at a scale Nepal cannot currently self-finance.

The irony, as the Eurasia Review analysis highlights, is that the most readily available source of capital for both solutions is China itself — creating a circular dependency that reinforces rather than resolves the structural imbalance.

Geopolitical Dimensions and Regional Context

Nepal's predicament is not isolated. Across South Asia and Southeast Asia, smaller BRI partner nations have faced similar patterns of trade asymmetry and infrastructure financing that disproportionately benefits Chinese firms. Sri Lanka's Hambantota Port and Pakistan's CPEC-linked debt burden are frequently cited as cautionary precedents in regional policy circles.

For Nepal, the challenge is compounded by its geography. Landlocked between India and China, Kathmandu has historically balanced its economic dependencies between the two giants. However, the rapid expansion of Chinese economic presence — through trade, BRI financing, and FDI — has shifted that balance in ways that Nepal's institutions are only beginning to formally document and resist.

India, Nepal's largest trading partner historically, remains a critical counterweight, but New Delhi's own trade and connectivity offers to Kathmandu have not always matched the scale or speed of Chinese engagement.

What Lies Ahead for Nepal

With Nepal's next budget cycle approaching and BRI project negotiations ongoing, the coming months will be critical in determining whether Kathmandu can renegotiate terms that allow greater participation by Nepali firms or diversify its economic partnerships meaningfully. International financial institutions, including the World Bank and Asian Development Bank, have signalled willingness to support alternative infrastructure financing — but political will within Nepal's fragmented coalition governments has historically been the binding constraint.

Unless structural reforms are implemented and alternative capital sources are mobilised, Nepal risks deepening its asymmetric economic dependence on China — a trajectory that its own central bank has already flagged as unsustainable.

Point of View

But ends up structurally dependent. The fact that Nepal's own Finance Ministry and central bank are now publicly documenting this risk is significant: it signals institutional alarm that political leadership has yet to translate into decisive action. What makes this particularly troubling is the circular trap — the only capital available to fix the problem is the same capital deepening it. India and multilateral lenders must recognise this window as a strategic opportunity to offer Nepal credible, transparent alternatives before the dependency becomes irreversible.

NationPress

2 Jul 2026

Frequently Asked Questions

What is Nepal's trade deficit with China in 2025?

In the first half of financial year 2025-26, Nepal's imports from China exceeded Rs 195 billion, while its exports to China were only a small fraction of that amount. This stark imbalance reflects a deepening structural trade deficit between the two countries.

How does the Belt and Road Initiative affect Nepal's economy?

Nepal joined China's Belt and Road Initiative in 2017, but World Bank data shows over 60 percent of BRI project contracts globally go to Chinese firms, limiting benefits for Nepali businesses. Domestic construction firms in Nepal are largely relegated to marginal roles while Chinese companies handle equipment and specialised engineering work.

Why can't Nepal reduce its dependence on Chinese imports?

Nepal's manufacturing sector is small and concentrated in food processing, textiles, and construction materials — sectors that directly compete with cheaper Chinese imports. Building domestic productive capacity requires capital investment at a scale Nepal cannot currently fund without external assistance.

Has Nepal's government acknowledged the risk of overdependence on China?

Yes, both Nepal's central bank and Finance Ministry have formally identified import dependence on China as a structural risk in their public planning documents. However, translating this institutional acknowledgement into concrete policy reforms has remained a challenge.

How does Nepal's situation compare to other BRI partner countries?

Nepal's experience mirrors patterns seen in other BRI recipient nations across South Asia and Southeast Asia, where trade asymmetry and infrastructure contracts disproportionately benefit Chinese firms. Sri Lanka's Hambantota Port and Pakistan's CPEC-related debt are frequently cited as cautionary examples in regional policy discussions.