What are the key changes in the Income Tax Bill 2025?

Synopsis

The Lok Sabha has passed the Income Tax Bill, 2025, transforming India's direct tax landscape. This new legislation aims to modernize tax provisions, enhance clarity, and promote taxpayer satisfaction. Key features include updated deduction rules and improved processes, setting the stage for a more efficient tax system. Discover how these changes impact investors and individuals alike.

Key Takeaways

New deductions for companies opting for the new tax regime.

Separation of MAT and AMT provisions for clarity.

Enhanced electronic payment options for professionals.

Streamlined processes for filing refund claims and tax returns.

Reduction in time for TDS correction statement filings.

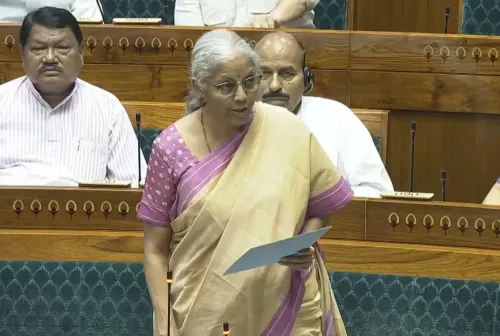

New Delhi, Aug 11 (NationPress) The Lok Sabha has successfully passed the Income Tax Bill, 2025, representing a crucial milestone in the effort to overhaul India's direct tax system, which has been in place for over six decades. The government aims to strike a balance between investor confidence, taxpayer relief, and administrative efficiency with this new legislation.

Upon enactment, this new law will replace the 63-year-old tax framework with a modernized set of regulations that reflect changing economic conditions.

Finance Minister Nirmala Sitharaman introduced the updated bill in Parliament, following the government’s choice to retract the earlier version submitted on February 13, 2025.

The previous draft had been referred to a Parliamentary Select Committee for consideration but was withdrawn on August 8 to eliminate confusion from multiple versions. The current bill consolidates all accepted amendments into a single, revised document.

The new draft integrates most of the 285 recommendations provided by the Select Committee, led by BJP MP Baijayant Panda. The committee presented its report on July 21, following a thorough review of the bill's provisions, with a focus on simplifying language, eliminating redundancies, and enhancing procedural clarity. It also proposed several drafting improvements, including alignment of phrases and corrections of cross-references.

Highlighted features of the Income Tax Bill, 2025 include:

- Deductions under Section 80M of the 1961 Act (Clause 148 of the IT Bill, 2025) are now accessible to companies opting for the new regime.

- Deductions for commuted pensions and gratuities for family members are included under Clause 93 of the 2025 bill.

- Provisions for Minimum Alternate Tax (MAT) and Alternate Minimum Tax (AMT) are now distinct sub-sections under Section 206.

- The AMT provisions apply solely to non-corporates claiming deductions; LLPs with only capital gains income are exempt if no deductions are claimed.

- The term 'profession' has been added after 'business' in clause 187, allowing professionals with total receipts exceeding Rs 50 crore annually the option of prescribed electronic payment methods.

- Flexibility has been introduced for filing refund claims where returns are submitted late, with Clause 263(1)(ix) being eliminated.

- The provisions concerning loss carry forward and set off have been redrafted for clarity while maintaining their original intent.

- The definition of receipt has been updated to reflect the concept of income, as per the existing act.

- Utilization of capital gains for acquiring new capital assets will be considered an application of income by registered non-profit organizations.

- In cases where regular income application is less than 85 percent due to late receipt, such income will be deemed as applied in the year it is derived, based on the taxpayer's choice.

- Taxation rules for anonymous donations have been aligned with current regulations, with exemptions for mixed-object registered non-profits.

- Mixed-object registered non-profit organizations are clearly defined.

- The requirement for mandatory investment and deposit of certain deemed accumulated income has been removed.

- Time for filing TDS correction statements has been reduced to two years from six years, potentially decreasing grievances among deductees.

- Necessary amendments from the Finance Act, 2025 and the Taxation Laws (Amendment) Bill, 2025 have been integrated into the new Bill.

The new law is set to be implemented starting April 1, 2026, replacing the Income Tax Act, 1961, which has been operational since April 1, 1962.

The government has introduced several major reforms since 2014, and the law has been amended to reflect updates in corporate tax, personal income tax, and capital gains taxation, among others.

Tax administration has become more efficient, transparent, and taxpayer-friendly, with improvements such as the Annual Information System that utilizes verified third-party data to pre-fill returns, centralized processing of returns, which has cut average processing time by 90% (to nearly 10 days), and faceless assessments to ensure impartiality and efficiency without physical barriers.

To minimize litigation, the Vivad se Vishwas scheme was introduced in 2020 and 2024, providing a means to settle longstanding tax disputes. Additionally, the limits for filing appeals in various forums have been increased.

Recent tax policy reforms include a 22 percent tax rate for companies that do not claim specific deductions and exemptions and a 15 percent rate for new manufacturing companies for a designated period. The new tax regime provides liberal slabs and lower rates, with increased rebates, meaning individuals earning up to Rs 12 lakh need not pay taxes under these provisions.

Presumptive tax provisions for non-residents have expanded to cover cruise shipping, raw diamonds, and services related to electronic manufacturing.

To encourage voluntary tax compliance, updated returns can now be filed up to four years after the end of the assessment year, and the period for reopening assessments has been limited to five years. Adjustments have also been made to the assessment of search cases.

Two separate regimes for trusts have been merged, which is a significant relief for non-profit organizations, while the capital gains taxation framework has been streamlined through the removal of indexation, rate reductions, and rationalization of holding periods.

Point of View

I view the passing of the Income Tax Bill, 2025 as a pivotal moment for India's economic future. This legislation not only modernizes our tax framework but also reflects the government's commitment to enhancing taxpayer experience and administrative efficiency. It balances investor needs with taxpayer relief, paving the way for a more robust economic environment.

NationPress

12 Aug 2026

Frequently Asked Questions

What are the main changes introduced in the Income Tax Bill 2025?

The Income Tax Bill 2025 introduces several key changes, including updated deduction rules, the separation of MAT and AMT provisions, and enhanced processes for filing tax returns. These changes aim to simplify tax administration and provide greater clarity for taxpayers.

When will the new Income Tax Bill come into effect?

The new Income Tax Bill will come into effect on April 1, 2026, replacing the existing Income Tax Act, 1961.

How does the new bill affect individual taxpayers?

The Income Tax Bill 2025 provides lower tax rates and increased rebates for individual taxpayers, particularly benefiting those earning up to Rs 12 lakh.

What reforms have been made to improve tax administration?

The government has implemented several reforms to enhance tax administration, including the Annual Information System, centralized processing of returns, and faceless assessments to ensure impartiality and efficiency.

Will there be changes to deductions for non-profit organizations?

Yes, the Income Tax Bill 2025 clarifies the provisions for non-profit organizations, particularly regarding anonymous donations and the merging of trust regimes.