Small savings scheme rates unchanged for July-September 2026 quarter

Synopsis

For another straight quarter, the Centre has left small savings rates untouched — SCSS and SSY lead at 8.2%, PPF holds at 7.1%, and NSC at 7.7%. With rates locked through September 2026, millions of risk-averse investors get predictability, but no upside surprise.

Key Takeaways

The Centre kept all small savings scheme interest rates unchanged for the July–September 2026 quarter.

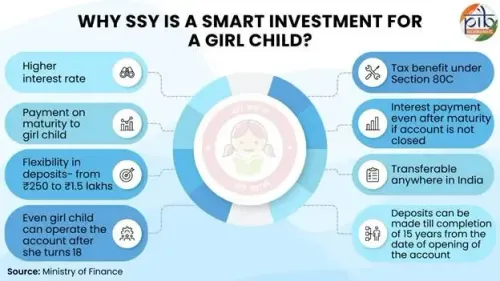

Senior Citizen Savings Scheme (SCSS) and Sukanya Samriddhi Yojana (SSY) offer the highest rate at 8.2% per annum.

Public Provident Fund (PPF) remains at 7.1% ; National Savings Certificate (NSC) at 7.7% ; POMIS at 7.4% .

Kisan Vikas Patra (KVP) retains 7.5% , maturing in 115 months .

Post Office Time Deposits range from 6.9% (1-year) to 7.5% (5-year); Recurring Deposit at 6.7% .

Rates are benchmarked to government securities yields and reviewed quarterly; next revision window is ahead of October–December 2026 .

The Centre on Tuesday, 30 June 2026 kept interest rates on all small savings schemes unchanged for the July–September quarter of FY2026-27, offering continued stability to millions of risk-averse investors who depend on government-backed instruments for predictable returns.

The Department of Economic Affairs under the Ministry of Finance issued a formal notification confirming that rates applicable from 1 July to 30 September 2026 will mirror those in effect during the April–June quarter. This marks yet another consecutive quarter of status quo on returns across the small savings basket.

Key Rates at a Glance

The Senior Citizen Savings Scheme (SCSS) and Sukanya Samriddhi Yojana (SSY) retain the highest annual return in the category at 8.2%. The National Savings Certificate (NSC) continues to yield 7.7% per annum, while the Public Provident Fund (PPF) holds steady at 7.1% per annum.

The Post Office Monthly Income Scheme (POMIS) will continue offering 7.4% annually, and Kisan Vikas Patra (KVP) retains its rate of 7.5%, with investments maturing in 115 months.

Post Office Time Deposit Rates

Rates on Post Office Time Deposits also remain untouched. One-year deposits earn 6.9%, two-year deposits 7%, three-year deposits 7.1%, and five-year deposits 7.5% annually. The five-year Post Office Recurring Deposit continues at 6.7% per annum.

Why the Government Held Rates Steady

Small savings rates are reviewed quarterly using a formula benchmarked to yields on government securities. However, revisions are not mandatory each quarter, and the government has exercised restraint in recent years — making only selective upward adjustments, notably for the SCSS and certain time deposits in earlier cycles.

This comes amid a broader monetary environment where the Reserve Bank of India (RBI) has been navigating rate decisions carefully. Keeping small savings rates stable helps the government manage its own borrowing costs, since these instruments are a significant source of public financing.

What This Means for Investors

Small savings schemes remain a cornerstone of household financial planning for millions of Indians, particularly senior citizens, rural savers, and those prioritising capital protection over market-linked returns. Several schemes — including the PPF, NSC, and SCSS — qualify for tax benefits under the Income Tax Act, reinforcing their appeal for long-term savings and retirement planning.

With rates held firm through at least September 2026, investors can plan their commitments with certainty for the coming quarter. Any revision will next be announced ahead of the October–December 2026 quarter.

Point of View

The government avoids upward pressure on its own borrowing costs — these instruments directly fund public expenditure. What is missing from the official narrative is any acknowledgement of real returns: with retail inflation still above 4%, a PPF rate of 7.1% offers a modest real yield, and the SCSS's 8.2% remains attractive only in the absence of better risk-free alternatives. The continued status quo also signals that the government sees no compelling reason — from either the bond market or the political calendar — to sweeten the deal. Savers should not expect a revision unless government securities yields shift materially in the next quarter.

NationPress

30 Jun 2026

Frequently Asked Questions

What are the current small savings scheme interest rates for July–September 2026?

The Centre has kept all rates unchanged from the previous quarter. Key rates include SCSS and SSY at 8.2%, NSC at 7.7%, PPF at 7.1%, POMIS at 7.4%, and KVP at 7.5%. Post Office Time Deposits range from 6.9% to 7.5% depending on tenure.

Why did the government keep small savings rates unchanged?

The government reviews rates quarterly based on a formula linked to government securities yields, but revisions are not mandatory. Holding rates steady also helps manage the government's own borrowing costs, as these schemes are a key source of public financing.

Which small savings scheme offers the highest interest rate?

The Senior Citizen Savings Scheme (SCSS) and Sukanya Samriddhi Yojana (SSY) both offer the highest rate in the category at 8.2% per annum for the July–September 2026 quarter.

When will small savings rates be reviewed next?

The next quarterly review will take place ahead of the October–December 2026 quarter. Any revision will be notified by the Department of Economic Affairs before 1 October 2026.

Do small savings schemes offer tax benefits?

Yes, several schemes including the PPF, NSC, and SCSS qualify for tax deductions under the Income Tax Act, making them popular choices for long-term savings and retirement planning in India.