What Does the Tax-Free Limit of Rs 12 Lakh Exclude?

Synopsis

In a recent budget announcement, the government declared a tax-free limit of Rs 12.75 lakh for taxpayers. However, certain incomes, especially capital gains, are excluded from this exemption. Discover how this impacts your finances and what you need to know about the Section 87A rebate.

Key Takeaways

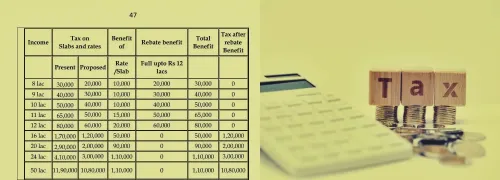

Tax-free income limit is set at Rs 12.75 lakh.

Standard deduction of Rs 75,000 applies under the new regime.

Short-term and long-term capital gains are excluded from the tax exemption.

Section 87A rebate is not applicable to special rate incomes.

Current tax utility does not allow Section 87A for special rate income.

New Delhi, Aug 16 (NationPress) In the recent Union Budget for 2025-26, the government revealed that individuals earning up to Rs 12.75 lakh, after accounting for a standard deduction of Rs 75,000, will enjoy a tax-free status under the updated tax regime.

It is crucial for taxpayers to recognize that both short-term and long-term capital gains taxes are excluded from the total income that qualifies for a complete exemption.

The Finance Act of 2025 has made it clear that the Section 87A rebate cannot be applied to income that is taxed at special rates. This means that taxpayers cannot use the Section 87A rebate to offset tax obligations arising from incomes taxed at special rates, such as short-term capital gains under Section 111A or long-term capital gains under Section 112A.

However, analysts point out that this change regarding the Section 87A rebate was instituted through an amendment in the Budget 2025, which will only take effect from the fiscal year 2025-26 (assessment year 2026-27). Presently, the Section 87A rebate on special rate incomes remains applicable for the fiscal year 2024-25 (assessment year 2025-26), as they observed.

For those unfamiliar, for assessment year 2025-26, taxpayers with a total annual income of up to Rs 7 lakh can avail the Section 87A rebate under the new tax framework, while individuals earning up to Rs 5 lakh are eligible under the old regime. In this scenario, a taxpayer's total income is computed by excluding exempt incomes and applying permissible deductions, which include the standard deduction for salary or pension earnings.

Utilizing the Section 87A rebate for incomes falling within the specified limits should lead to a net tax liability of zero.

However, the current Income Tax Return utility does not allow the Section 87A rebate on taxes calculated for special rate incomes for the fiscal year 2024-25. Consequently, individuals with total incomes below Rs 7 lakh may still face tax liabilities if their primary income source is through special-rate capital gains. Analysts are awaiting additional clarification from the Income Tax Department regarding whether this law will have a retrospective effect from the fiscal year 2024-25.

Point of View

It is essential to highlight the ongoing complexities in tax regulations that impact a significant portion of taxpayers. The recent changes from the Union Budget 2025-26 require careful consideration and understanding to navigate effectively. NationPress remains committed to keeping the public informed about these financial developments.

NationPress

8 Jul 2026

Frequently Asked Questions

What is the tax-free limit announced in the Union Budget 2025-26?

The government announced a tax-free limit of Rs 12.75 lakh for the year 2025-26.

Are capital gains included in the tax-free income?

No, short-term and long-term capital gains are not included in the income that qualifies for the tax-free limit.

What is the Section 87A rebate?

The Section 87A rebate allows eligible taxpayers to reduce their tax liability, but it cannot be applied to income taxed at special rates.

Who qualifies for the Section 87A rebate?

Taxpayers with an annual total income of up to Rs 7 lakh under the new tax regime can qualify for the Section 87A rebate.

Will the changes in Section 87A affect past fiscal years?

The recent amendments will take effect from FY 2025-26 onwards and will not apply retroactively to FY 2024-25.