Nil Tax Threshold Raised to Rs 12 Lakh: Taxpayers Set to Gain from Budget 2025-26 Changes

Synopsis

The recent announcement by Finance Minister Nirmala Sitharaman about raising the nil tax threshold to Rs 12 lakh is a significant benefit for middle-class taxpayers, eliminating their tax obligations under the new regime. This change is expected to impact around one crore individuals, providing substantial financial relief.

Key Takeaways

Nil tax for incomes up to Rs 12 lakh.

Previous threshold was Rs 7 lakh.

Standard deduction of Rs 75,000 applies.

Affects around one crore taxpayers.

New tax regime is now the default.

New Delhi, Feb 1 (NationPress) The significant announcement made by Finance Minister Nirmala Sitharaman regarding the income tax bracket for earnings up to Rs 12 lakh has elicited jubilant reactions among the middle-class and taxpayers.

By eliminating their tax burden entirely, FM Sitharaman revealed this generous measure when it was least anticipated. However, these modifications apply solely to the New Tax Regime.

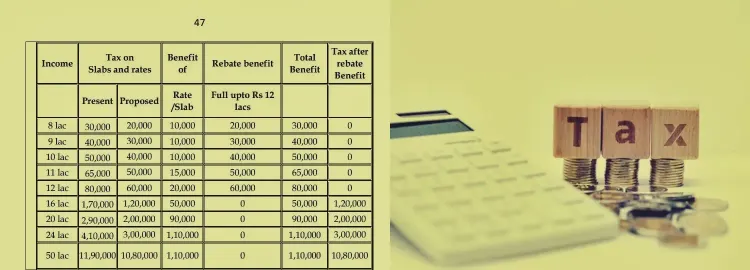

According to the proposed alterations in the Union Budget 2025-26, individuals earning up to Rs 12 lakh will no longer be obligated to pay any income tax, marking a substantial change from the prior system where they had to remit between Rs 60,000 and Rs 80,000.

"The New Tax Regime is the standard framework. To benefit from the rebate permitted under the new provisions, only a tax return needs to be submitted; no additional actions are necessary," stated an official announcement.

Moreover, a standard deduction of Rs 75,000 is available to taxpayers within this new regime. Consequently, a salaried individual will not be liable for any taxes if their income before the standard deduction is less than or equal to Rs 12,75,000.

Here are some Q&As concerning the new income tax slabs:

What was the previous income threshold for nil tax?

Previously, the income threshold for nil tax was Rs 7 lakh. By raising this threshold to Rs 12 lakh, approximately one crore taxpayers who were earlier required to pay taxes ranging from Rs 20,000 to Rs 80,000 will now pay no tax.

Who will gain from the modification of tax slabs?

The new tax regime applies to individuals, Hindu undivided families, associations of persons [excluding co-operative societies], bodies of individuals, whether incorporated or not, or artificial juridical entities as outlined in sub-clause (vii) of clause (31) of section 2.

Thus, the adjustments in tax slabs will benefit all these entities.

What advantages can a taxpayer avail?

Any individual who previously had to pay Rs 80,000 in taxes (under the new regime) for an income of Rs 12 lakh will now be exempt from tax on that income.