FM Sitharaman: GST reforms cut rates on household essentials

Synopsis

On the ninth anniversary of GST, Finance Minister Nirmala Sitharaman said next-generation reforms have cut rates on essential household items, making daily purchases more affordable and simplifying the tax structure for businesses and consumers alike.

Key Takeaways

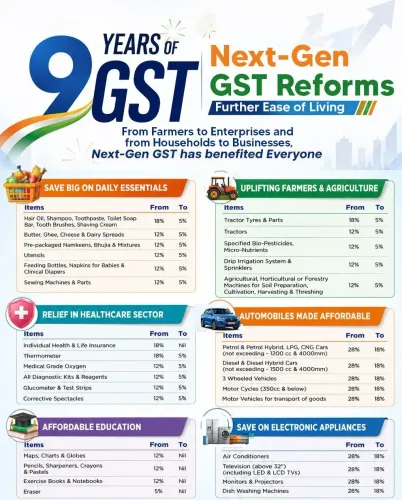

1 July 2026 marks the ninth anniversary of the Goods and Services Tax, launched on 1 July 2017 .

Finance Minister Nirmala Sitharaman says 'Next-Gen GST reforms' have reduced rates on several essential household items.

The GST Council , comprising central and state finance ministers, is the constitutional body that approves all rate changes.

Previous rounds of rate rationalisation were undertaken in 2019 and 2022 , targeting essentials and high-compliance-burden categories.

Key stakeholders include households, FMCG retailers, and state governments that share GST revenue.

The next GST Council meeting and forthcoming economic documents are expected to detail the revenue and structural impact of current reforms.

Union Finance Minister Nirmala Sitharaman on Wednesday, 1 July 2026 marked nine years of the Goods and Services Tax by highlighting that next-generation GST reforms have lowered rates on several essential household items, easing the cost of everyday purchases while streamlining the broader tax structure.

Context

The post, shared on the occasion of #9YearsOfGST, underscores the government's position that the unified indirect tax regime has matured well beyond its foundational rollout. GST was introduced on 1 July 2017, replacing a complex web of central and state levies — excise duty, VAT, service tax, and several others — with a single, constitutionally backed framework. The anniversary has become an annual occasion for the Finance Ministry to communicate the tax's evolving consumer benefits.

Sitharaman, who has overseen GST policy as Finance Minister since 2019, framed the reforms around two distinct outcomes: affordability for households and administrative simplicity for businesses and tax authorities alike.

Policy Backdrop

The GST Council — the constitutional body comprising the Union Finance Minister and state finance ministers — has been the primary vehicle for rate rationalisation since the tax's inception. Multiple rounds of revisions, including significant adjustments in 2019 and 2022, have progressively moved essential goods toward lower slabs or exemption, responding to inflationary pressures and calls from trade bodies and consumer groups.

The broader pattern across nine years has been one of incremental reform: narrowing the number of items in higher slabs, bringing more transactions under the formal economy, and improving compliance through technology-driven return filing and invoice matching. The government has consistently described rate rationalisation on essentials as a tool for both inflation management and formalisation of the supply chain.

The phrase 'Next-Gen GST reforms' used in Sitharaman's post signals a continued policy push beyond the foundational architecture — potentially encompassing compliance simplification, digital integration, and further slab restructuring, though specifics of the current round are subject to formal GST Council announcements.

Stakeholders and Impact

The most direct beneficiaries of rate reductions on household essentials are ordinary consumers, particularly in lower and middle-income brackets where FMCG spending constitutes a significant share of monthly budgets. Lower GST on items such as food products, personal care goods, and daily-use commodities translates, in principle, to lower shelf prices — provided the benefit is passed on by retailers and manufacturers.

FMCG retailers and manufacturers also benefit from a simpler rate structure, which reduces compliance costs and the risk of classification disputes. For small traders, a rationalised slab system eases the burden of determining applicable rates across diverse product categories.

State governments, which share GST revenues, remain key stakeholders in any rate revision, as reductions affect the common pool. The GST Council's consensus-based mechanism ensures that states are party to any such decisions, lending them political and fiscal legitimacy.

What's Next

Attention will now turn to the next GST Council meeting, where the specifics of any further rate changes or structural reforms are expected to be formalised. Any revenue-impact assessment of the current round of reductions is likely to feature in forthcoming government economic documents. With the tax completing its ninth year, calls for a comprehensive review of the four-slab structure — and a possible move toward fewer, rationalised rates — are expected to grow louder among economists and industry bodies.

The government's ability to balance revenue buoyancy with consumer relief will remain the central tension as GST enters its next phase of evolution.

Point of View

Framing nine years of GST not as a static achievement but as a living, reforming system — a narrative the BJP has consistently deployed to counter criticism that the original rollout was rushed and regressive on essentials. The emphasis on 'Next-Gen' reforms signals that the government intends to keep GST rationalisation as a visible policy deliverable ahead of budget cycles. By tying rate cuts to household affordability, the Finance Ministry is also addressing a politically sensitive pressure point: the cost of living. The post fits a broader arc in which the GST Council mechanism is positioned as cooperative federalism in action, even as centre-state tensions over revenue sharing periodically resurface.

NationPress

1 Jul 2026

Frequently Asked Questions

What are the Next-Gen GST reforms Nirmala Sitharaman mentioned?

Finance Minister Nirmala Sitharaman used the term 'Next-Gen GST reforms' to describe the latest round of rate reductions on essential household items and simplification of the tax structure, announced on the ninth anniversary of GST on 1 July 2026. Specific details of the current round are subject to formal GST Council announcements.

Which household items have seen GST rate cuts?

The Finance Minister's post states that several essential household items have seen rate reductions under the latest GST reforms, making everyday purchases more affordable. Exact product categories are determined by the GST Council and formally notified; previous rounds covered food products, personal care items, and daily-use goods.

When was GST launched in India?

GST was launched in India on 1 July 2017 , replacing multiple central and state indirect taxes including excise duty, VAT, and service tax with a unified, constitutionally backed framework.

What is the GST Council and who is part of it?

The GST Council is a constitutional body comprising the Union Finance Minister and the finance ministers of all state and union territory governments. It recommends GST rates, exemptions, and structural changes, operating on a consensus basis to reflect cooperative federalism.

How has GST changed over nine years?

Over nine years, GST has undergone multiple rounds of rate rationalisation — notably in 2019 and 2022 — moving essential goods to lower slabs or exemptions, improving compliance through digital return filing and invoice matching, and progressively formalising the supply chain. The government describes this as an ongoing evolution toward a simpler, more equitable indirect tax system.