Who Are the Rightful Owners Claiming Over Rs 2,000 Crore in the ‘Your Money, Your Right’ Campaign?

Synopsis

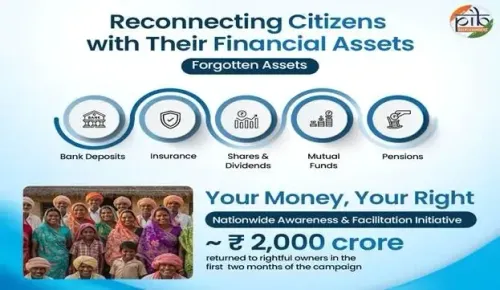

The ‘Your Money, Your Right’ campaign has led to over Rs 2,000 crore being reclaimed by rightful owners in just two months. Launched on October 4, this initiative aims to recover unclaimed financial assets for the public. Discover how this extensive campaign is changing lives and promoting financial awareness.

Key Takeaways

Campaign launched on October 4 .

Rs 2,000 crore reclaimed in two months .

Involves multiple financial regulators .

Focus on public awareness and accessibility .

Empowers citizens to recover unclaimed assets .

New Delhi, Dec 9 (NationPress) Following the launch of a nationwide initiative named ‘Your Money, Your Right’ on October 4, aimed at helping individuals reclaim unclaimed financial assets such as bank deposits, insurance payouts, dividends, shares, mutual funds, and pensions, approximately Rs 2,000 crore has been claimed by rightful owners within the first two months, as reported to Parliament on Tuesday.

The Minister of State for Finance, Pankaj Chaudhary, provided this information in a written response during a Rajya Sabha session, explaining that the campaign operates under the 3A Framework — Awareness, Accessibility, and Action. This three-month campaign (October–December 2025) is being rolled out in every state and Union Territory.

“From October to December 5, 2025, camps were organized in 477 districts with the involvement of public representatives, local administration, and officials from financial institutions,” he added.

To enhance outreach during the campaign, comprehensive standard operating procedures (SOPs), frequently asked questions (FAQs), and awareness materials in key regional languages—along with engaging short video messages—have been extensively shared. Camps at the district level provide on-ground digital demonstrations, helpdesks, and guided assistance to streamline the claims process, he noted.

This campaign is a collaborative effort involving all significant financial sector regulators, including the Reserve Bank of India (RBI), Securities and Exchange Board of India (SEBI), Insurance Regulatory and Development Authority of India (IRDAI), Pension Fund Regulatory and Development Authority (PFRDA), and the Investor Education and Protection Fund Authority (IEPFA).

Existing platforms such as the RBI’s UDGAM (for unclaimed bank deposits), the IRDAI’s Bima Bharosa (for unclaimed insurance proceeds), and the SEBI’s MITRA (for unclaimed mutual funds) have significantly aided citizens in tracking down their unclaimed assets.

Previously, the minister disclosed in Parliament that Indian banks have resolved over Rs 10,000 crore worth of unclaimed deposits over the past three years.

In a written statement to the Rajya Sabha, Chaudhary noted that both public and private banks have returned thousands of dormant or forgotten accounts to rightful claimants from April 2022 to November 2025.

According to the RBI's Depositor Education and Awareness (DEA) Fund Scheme, banks must transfer balances from savings, current, and term deposit accounts that go unclaimed for 10 years to a central fund overseen by the apex bank.

As of June 30 this year, public sector banks transferred over Rs 58,000 crore to this fund, with the State Bank of India contributing Rs 19,330 crore alone. Private banks have added around Rs 9,000 crore to the DEA Fund, led by ICICI Bank, HDFC Bank, and Axis Bank.

Point of View

It is crucial to highlight that the success of the 'Your Money, Your Right' campaign reflects the government's commitment to financial inclusivity. By enabling citizens to reclaim their unclaimed assets, we are fostering a more equitable financial environment. This initiative not only empowers individuals but also strengthens the overall economy.

NationPress

14 Jul 2026

Frequently Asked Questions

What is the 'Your Money, Your Right' campaign?

The 'Your Money, Your Right' campaign is a government initiative aimed at helping individuals reclaim unclaimed financial assets such as bank deposits, insurance, dividends, shares, mutual funds, and pensions.

How much money has been reclaimed so far?

In its first two months, approximately Rs 2,000 crore has been claimed by rightful owners under this campaign.

Which financial regulators are involved in this campaign?

The campaign involves major financial sector regulators including the Reserve Bank of India (RBI), Securities and Exchange Board of India (SEBI), Insurance Regulatory and Development Authority of India (IRDAI), Pension Fund Regulatory and Development Authority (PFRDA), and Investor Education and Protection Fund Authority (IEPFA).

How can individuals trace their unclaimed assets?

Individuals can utilize platforms like the RBI’s UDGAM for unclaimed bank deposits and IRDAI’s Bima Bharosa for unclaimed insurance proceeds to trace their assets.

What is the significance of this campaign?

This campaign enhances financial awareness and accessibility, enabling rightful owners to reclaim their unclaimed assets effectively.