Sitharaman: Credit Guarantee schemes ended vendor exploitation

Synopsis

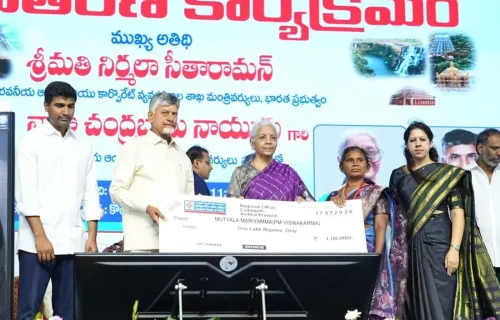

Union Finance Minister Nirmala Sitharaman, speaking in Narasaraopeta, Andhra Pradesh on 17 July 2026, said PM Modi's government-backed credit guarantee vision transformed access to formal finance for vendors, artisans, fishermen and farmers who once depended on exploitative moneylenders.

Key Takeaways

Finance Minister Nirmala Sitharaman spoke at Narasaraopeta, Andhra Pradesh on 17 July 2026 on credit access for informal-sector workers.

She credited PM Narendra Modi with envisioning a 'Government-backed Credit Guarantee framework' after she described the plight of small vendors to him.

PM SVANidhi (launched June 2020 ) and Pradhan Mantri Mudra Yojana (launched April 2015 , loans up to Rs 10 lakh ) are the flagship schemes underpinning this framework.

Beneficiary groups named include street vendors, artisans, fishermen and farmers — segments historically reliant on informal moneylenders.

Banks have been directed to conduct outreach camps rather than wait for customers, expanding last-mile credit delivery.

Disbursement and recovery data in upcoming RBI quarterly reports and the next Union Budget will indicate the framework's trajectory.

Union Finance Minister Nirmala Sitharaman on Friday, 17 July 2026, speaking at Narasaraopeta, Andhra Pradesh, recalled how exploitative informal credit once trapped small vendors and described how a conversation with Prime Minister Narendra Modi led to the creation of government-backed credit guarantee frameworks that now extend formal finance to vendors, artisans, fishermen and farmers.

Context

Addressing the gathering in Narasaraopeta, Sitharaman said she had personally witnessed small vendors depending on 'exploitative informal credit just to keep their businesses running.' She credited PM Modi with envisioning a 'Government-backed Credit Guarantee framework to make affordable institutional credit accessible.' The minister underlined that beneficiaries can now 'access formal finance with dignity' — a phrase that signals the government's framing of financial inclusion as a rights-based outcome, not merely a welfare measure.

She also noted that under Modi's leadership, banks have been 'encouraged to go to the people, not wait for people to come to them' — a reference to outreach camps and doorstep banking initiatives that public sector banks have expanded in recent years.

Policy Backdrop

The credit guarantee architecture Sitharaman referenced has been built in layers over the past decade. The Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE), operational since 2000, reduced collateral requirements for small borrowers. Pradhan Mantri Mudra Yojana (PMMY), launched in April 2015, extended collateral-free loans of up to Rs 10 lakh to non-farm micro enterprises including vendors and artisans.

The Pradhan Mantri Street Vendor's AtmaNirbhar Nidhi (PM SVANidhi), introduced in June 2020, provided working capital loans specifically to street vendors with government credit guarantee cover. Together, these schemes form the backbone of the formalisation push that Sitharaman described — shifting borrowers away from moneylenders and towards regulated institutional lenders.

The broader financial inclusion drive since 2014 has combined Jan Dhan accounts, Aadhaar linkage, and digital payments to create the rails on which credit guarantee schemes now run. Simplified KYC norms and direct benefit transfers have further reduced friction for first-time borrowers in rural and semi-urban areas.

Stakeholders and Impact

The four beneficiary groups Sitharaman named — vendors, artisans, fishermen and farmers — represent a large share of India's informal workforce, which has historically relied on moneylenders charging usurious rates. Access to institutional credit at regulated interest rates directly lowers the cost of working capital and reduces debt-trap risk for these groups.

Public sector banks, directed to expand outreach through camps and simplified processes, bear the operational burden of this shift. The credit guarantee cover provided by the government reduces banks' risk exposure, making it commercially viable for them to lend to borrowers without traditional collateral. Fishermen and artisans, who often lack land titles or formal income proof, stand to benefit most from this risk-sharing model.

What's Next

The health of these guarantee frameworks will be tracked through disbursement and recovery data in upcoming quarterly reports from the Reserve Bank of India. Any fresh allocation or expansion of guarantee cover in the next Union Budget will be a key indicator of the government's continued commitment to this agenda. Sitharaman's remarks in Andhra Pradesh also signal continued political outreach to beneficiary communities ahead of the legislative calendar, reinforcing the government's narrative around inclusive growth and economic dignity.

Point of View

Signalling continued outreach in a state where the BJP-TDP alliance is consolidating its base. The 'dignity' framing of credit access is a deliberate upgrade from the welfare narrative, positioning the government's financial inclusion record as an empowerment story ahead of what is likely to be a budget-heavy political season. Analysts will watch whether fresh guarantee allocations in the next Union Budget back up the rhetorical commitment with fiscal muscle.

NationPress

17 Jul 2026

Frequently Asked Questions

What is the PM SVANidhi scheme?

PM SVANidhi — Pradhan Mantri Street Vendor's AtmaNirbhar Nidhi — is a scheme launched in June 2020 that provides collateral-free working capital loans to street vendors, backed by a government credit guarantee to reduce lender risk.

What did Nirmala Sitharaman say in Narasaraopeta?

Speaking in Narasaraopeta, Andhra Pradesh on 17 July 2026 , Sitharaman said she had seen small vendors trapped by exploitative informal credit and that PM Modi envisioned a government-backed credit guarantee framework to give vendors, artisans, fishermen and farmers access to affordable formal finance.

What is Pradhan Mantri Mudra Yojana?

Pradhan Mantri Mudra Yojana (PMMY) , launched in April 2015 , offers collateral-free loans of up to Rs 10 lakh to non-farm micro enterprises including small vendors and artisans, under a government credit guarantee framework.

How has India reduced dependence on moneylenders for small businesses?

Since 2014 , India has combined Jan Dhan accounts, Aadhaar linkage, digital payments and credit guarantee schemes such as PMMY and PM SVANidhi to shift informal-sector borrowers from moneylenders to regulated institutional lenders at lower interest rates.

What is the Credit Guarantee Fund Trust for Micro and Small Enterprises?

The Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) , operational since 2000 , provides guarantee cover on loans to micro and small enterprises, reducing the collateral burden on borrowers and the credit risk for lenders.