Lok Sabha Greenlights Amendment to Insolvency and Bankruptcy Code

Synopsis

The Lok Sabha's recent approval of the Insolvency and Bankruptcy Code (Amendment) Bill marks a significant step toward expediting the resolution of insolvency cases, with Finance Minister Nirmala Sitharaman highlighting its importance in improving corporate governance and banking health.

Key Takeaways

14-day timeline for insolvency application admissions.

Introduction of penalties to deter misuse of the process.

Emphasis on improving the banking sector's health .

Focus on enhancing corporate governance for companies.

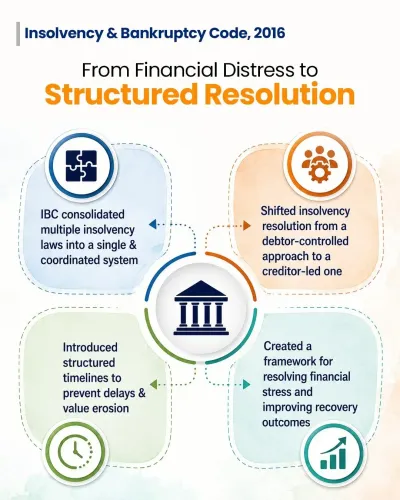

IBC serves to resolve stressed assets, not just recover debts.

In New Delhi, on March 30, the Lok Sabha has officially approved the Insolvency and Bankruptcy Code (Amendment) Bill, which is designed to expedite insolvency processes for companies that have defaulted.

This legislation mandates a 14-day deadline for the acceptance of insolvency applications once a company's default is confirmed.

Finance Minister Nirmala Sitharaman indicated that the government is introducing a series of 12 amendments aimed at bolstering the resolution framework.

She pointed out that the main cause of delays in IBC resolutions stems from prolonged litigation, and the new Bill includes penalties to deter misuse of the process.

The Lok Sabha discussed the Bill, which was proposed by Finance Minister Nirmala Sitharaman, on March 27. Initially referred to a Select Committee, the Bill addresses the issues surrounding delays in insolvency and bankruptcy case resolutions.

During her address in the Lower House, Sitharaman emphasized that the Insolvency and Bankruptcy Code (IBC) has significantly enhanced the banking sector's health, asserting that the law was not merely intended to serve as a debt recovery mechanism.

While presenting the Bill, the finance minister stated that the IBC has fostered improved credit discipline and has positively influenced the credit profiles of corporations.

She noted that companies that have undergone the insolvency resolution process have exhibited better performance and enhanced corporate governance practices.

In her remarks about the Insolvency and Bankruptcy Code (Amendment) Bill, 2025, as reported by the Select Committee, Sitharaman stated, “The Insolvency and Bankruptcy Code, enacted in 2016, has been pivotal in enhancing the overall health of the Indian banking sector,” adding that the framework has enabled companies to achieve improved credit ratings.

She clarified that the primary aim of this law is to resolve stressed assets rather than solely recover debts. “The IBC serves as a framework for rescuing viable businesses and addressing financial distress while maintaining enterprise value. It was never designed to be a tool for debt collection,” she elaborated.

Point of View

The approval of the Insolvency and Bankruptcy Code (Amendment) Bill by the Lok Sabha represents a critical development in India's financial landscape. By addressing the delays in the insolvency process, this legislation aims to strengthen the resolution framework for distressed companies, ultimately benefiting the banking sector and enhancing corporate governance practices across the board.

NationPress

30 Jun 2026

Frequently Asked Questions

What is the purpose of the Insolvency and Bankruptcy Code (Amendment) Bill?

The Bill aims to speed up insolvency proceedings for defaulting companies by introducing a mandatory 14-day timeline for admitting insolvency applications.

Who introduced the Insolvency and Bankruptcy Code (Amendment) Bill?

The Bill was introduced by Finance Minister Nirmala Sitharaman.

What are the key features of the Bill?

The Bill includes a 14-day deadline for insolvency application admissions and proposes penalties to prevent the misuse of the insolvency process.

How has the IBC impacted the banking sector?

The IBC has significantly improved the health of the banking sector by enhancing credit discipline and the credit profiles of companies.

Is the IBC intended for debt recovery?

No, the IBC is designed to resolve stressed assets and rescue viable businesses rather than serve as a tool for debt recovery.