Joshi: Solar capacity up 46 GW in a year, non-fossil at 297 GW

Synopsis

Union Minister Pralhad Joshi announced on 9 July 2026 that India's solar installed capacity grew from 116.25 GW to 162.15 GW in one year and total non-fossil fuel capacity reached 297.36 GW, marking significant progress toward the 500 GW Panchamrit target by 2030.

Key Takeaways

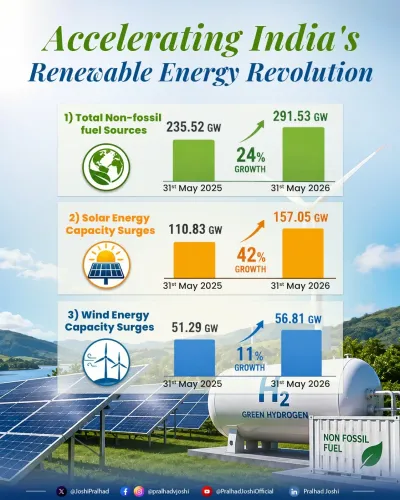

India's installed solar capacity rose from 116.25 GW to 162.15 GW in a single year — a net addition of nearly 46 GW .

Total non-fossil fuel capacity increased from 242.78 GW to 297.36 GW , a gain of approximately 54.58 GW .

The figures were shared by Union Minister Pralhad Joshi on 9 July 2026 , attributing the progress to PM Modi's leadership.

India's Panchamrit target requires 500 GW of non-fossil fuel capacity by 2030 ; roughly 202.64 GW still needs to be added.

The Ministry of New and Renewable Energy , headed by Joshi, oversees policy and programme implementation for the transition.

Key policy instruments include competitive bidding, payment security mechanisms, and the Production Linked Incentive scheme for domestic manufacturing.

Union Consumer Affairs and New and Renewable Energy Minister Pralhad Joshi on Thursday, 9 July 2026 shared data showing India's installed solar capacity has surged from 116.25 GW to 162.15 GW in a single year, while total non-fossil fuel capacity climbed from 242.78 GW to 297.36 GW, underscoring the country's accelerating clean energy transition.

Context

In his post, Minister Joshi credited the momentum to the leadership of Prime Minister Narendra Modi, stating that India is 'accelerating towards its clean energy goals with speed, scale and determination — building a greener, more sustainable future for generations to come.' The figures represent a net addition of nearly 46 GW in solar alone over the year, and a gain of roughly 54.58 GW in overall non-fossil fuel capacity.

The announcement comes as India's power sector continues to attract large-scale investment in solar parks, rooftop installations, and hybrid renewable projects. The pace of addition, if sustained, would place the country on a steeper trajectory toward its long-term climate targets.

Policy Backdrop

India's renewable energy ambitions are anchored in the Panchamrit framework, a five-point climate commitment announced by Prime Minister Modi at the COP26 summit in Glasgow in 2021. The centrepiece target is 500 GW of non-fossil fuel capacity by 2030, alongside a pledge to achieve net-zero emissions by 2070.

The policy lineage stretches back to the Jawaharlal Nehru National Solar Mission, launched in 2010 with an initial target of 20 GW that was revised upward multiple times as costs fell and deployment accelerated. India also co-founded the International Solar Alliance in 2015 to drive global solar adoption, particularly among sun-belt nations.

Competitive bidding, payment security mechanisms for project developers, and manufacturing incentives under the Production Linked Incentive scheme have been the principal domestic instruments driving capacity growth.

Stakeholders and Impact

Renewable energy project developers and state electricity utilities are the most directly affected stakeholders. Faster capacity addition increases the volume of power purchase agreements utilities must manage, while also placing pressure on grid integration and storage infrastructure to handle variable generation.

For consumers, a larger share of non-fossil generation in the mix has implications for long-run electricity tariffs and energy security. India's rising electricity demand — driven by industrial growth, cooling loads, and electrification of transport — makes the pace of renewable addition a macro-economic variable as much as a climate one.

The Ministry of New and Renewable Energy, which Joshi heads alongside his Consumer Affairs portfolio, is the nodal body overseeing policy, target-setting, and programme implementation for this transition.

What's Next

With non-fossil capacity now at 297.36 GW, India needs to add approximately 202.64 GW more to reach the 500 GW Panchamrit target by 2030 — a significant but not unprecedented challenge given recent annual addition rates. The next quarterly capacity addition report from the Ministry of New and Renewable Energy will be closely watched to gauge whether the current trajectory is holding.

Any fresh renewable energy targets or financing provisions in the forthcoming Union Budget could further shape the pace and structure of India's clean energy build-out, making the sector one of the more consequential arenas in domestic economic policy over the next four years.

Point of View

If verified in official quarterly data, would be among the fastest annual increments India has recorded and strengthens the government's negotiating posture in multilateral climate forums. Posting the figures under the Panchamrit and CleanEnergy hashtags signals a deliberate effort to link domestic capacity milestones to the broader international narrative of India as a credible climate actor. The emphasis on 'speed, scale and determination' also sets a rhetorical baseline against which the ministry's performance will be measured as the 2030 deadline approaches.

NationPress

9 Jul 2026

Frequently Asked Questions

What is India's current solar installed capacity as of 2026?

According to Union Minister Pralhad Joshi's post on 9 July 2026, India's installed solar capacity stands at 162.15 GW , up from 116.25 GW a year earlier.

What is India's 500 GW renewable energy target and when is the deadline?

India's Panchamrit framework, announced by PM Modi at COP26 in 2021, sets a target of 500 GW of non-fossil fuel capacity by 2030 . Total non-fossil capacity currently stands at 297.36 GW, leaving roughly 202.64 GW to be added.

Who is Pralhad Joshi and which ministry does he head?

Pralhad Joshi is a senior BJP leader from Karnataka who serves as Union Minister for Consumer Affairs, Food and Public Distribution, and also heads the Ministry of New and Renewable Energy .

What is the Panchamrit climate commitment India made at COP26?

The Panchamrit is a five-point climate pledge announced by PM Modi at the COP26 summit in Glasgow in 2021 . It includes achieving 500 GW non-fossil fuel capacity by 2030, meeting 50 percent of energy needs from renewables by 2030, and reaching net-zero emissions by 2070.

How much solar capacity did India add in one year according to the minister?

Minister Joshi's post states that India added approximately 46 GW of solar capacity in one year, growing from 116.25 GW to 162.15 GW.