Sitharaman Highlights Banking Reforms, Credit Access in AP

Synopsis

Finance Minister Nirmala Sitharaman, addressing an audience in Narasaraopeta, Andhra Pradesh, credited the Credit Guarantee framework and a decade of banking reforms under PM Modi with extending institutional credit to street vendors and first-time entrepreneurs previously shut out of the formal financial system.

Key Takeaways

Finance Minister Nirmala Sitharaman spoke at Narasaraopeta, Andhra Pradesh on 17 July 2026 on banking reforms since 2014 .

She highlighted the Credit Guarantee framework as the principal instrument enabling first-time entrepreneurs and street vendors to access institutional credit without collateral.

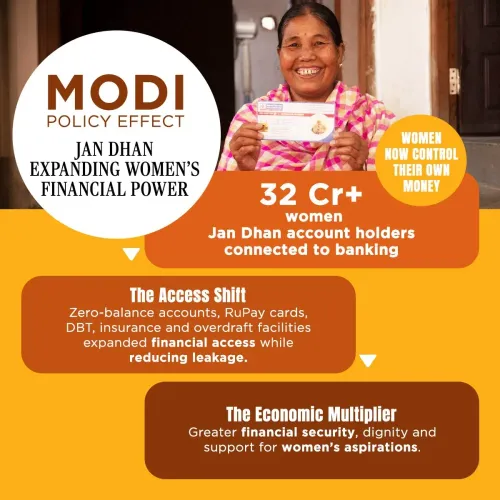

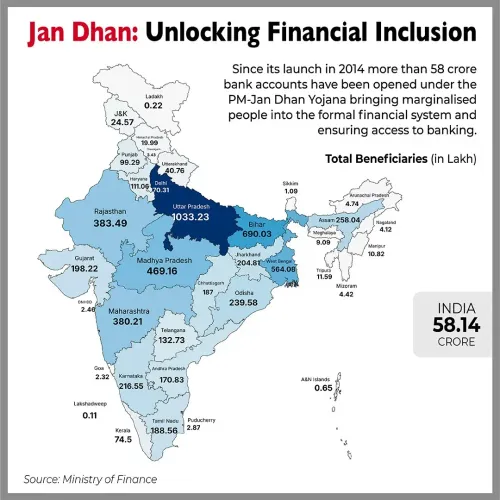

Pradhan Mantri Jan Dhan Yojana (August 2014), MUDRA Yojana (April 2015, loans up to ₹10 lakh ), and PM SVANidhi (June 2020) form the three-pillar policy foundation she referenced.

Structural banking reforms — including the Insolvency and Bankruptcy Code 2016 and public-sector bank consolidation — have underpinned the healthier banking system she cited.

The government's stated emphasis has shifted from supply-side inclusion targets (account-opening) to demand-side credit delivery for those 'who need it most.' Next Union Budget allocations for credit guarantee funds and Andhra Pradesh's own policy response are the key developments to watch.

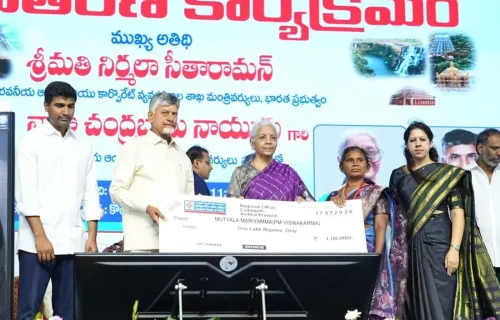

Union Finance Minister Nirmala Sitharaman on Friday, 17 July 2026, spoke at Narasaraopeta, Andhra Pradesh, crediting the decade since 2014 with a fundamental transformation of India's banking landscape under Prime Minister Narendra Modi. She underscored how the government's Credit Guarantee framework has opened institutional credit to first-time entrepreneurs and street vendors who were previously excluded from the formal financial system.

Context

Addressing her audience in Narasaraopeta, Sitharaman said that since 2014, the government has worked to advance a vision of 'reaching every village and every citizen.' She noted that a 'stronger banking system now serves those who need it most,' framing financial inclusion not merely as account-opening but as the delivery of actual credit to underserved borrowers.

The remarks reflect a deliberate shift in the government's narrative — from counting bank accounts opened to measuring credit actually disbursed to informal-sector participants such as street vendors and first-generation business owners.

Policy Backdrop

The architecture Sitharaman referenced rests on three successive policy pillars. Pradhan Mantri Jan Dhan Yojana, launched in August 2014, gave zero-balance bank accounts and insurance cover to millions of unbanked households. MUDRA Yojana, introduced in April 2015, extended micro-credit of up to ₹10 lakh to non-corporate small businesses. PM SVANidhi, announced in June 2020, provided collateral-free working-capital loans specifically to street vendors.

Running alongside these inclusion drives were structural banking reforms — the Insolvency and Bankruptcy Code of 2016 and a consolidation of public-sector banks — aimed at building a healthier balance-sheet foundation from which expanded lending could be sustained. The Credit Guarantee framework ties these strands together by absorbing default risk on behalf of borrowers who lack collateral, making lenders willing to extend credit to segments they would otherwise avoid.

Stakeholders and Impact

Street vendors, first-time entrepreneurs, and unbanked rural households are the primary beneficiaries Sitharaman highlighted. For these groups, the absence of collateral has historically been the single largest barrier to borrowing from a bank or a regulated lender. Credit guarantees effectively substitute sovereign backing for personal assets, lowering the risk premium lenders charge.

The Andhra Pradesh setting is significant: the state has a large agrarian and small-trade economy, and Narasaraopeta — a parliamentary constituency in the state's interior — represents exactly the kind of semi-urban, mixed-economy constituency where Jan Dhan accounts and MUDRA loans have had measurable penetration. Any further state-level adoption of credit guarantee frameworks by the Andhra Pradesh government could deepen this reach.

What's Next

Attention will now turn to the next Union Budget cycle and whether allocations to credit guarantee funds are expanded to reflect the government's stated ambition of demand-side credit delivery rather than supply-side account targets. Analysts will also watch whether Andhra Pradesh's state government moves to complement central schemes with its own credit-support mechanisms for micro-entrepreneurs.

Sitharaman's appearance in Narasaraopeta signals continued political investment in the financial-inclusion narrative ahead of future electoral cycles, with the BJP seeking to consolidate its outreach among informal-economy workers and first-generation borrowers across southern India.

Point of View

The Finance Ministry is signalling a maturation of the inclusion agenda: the argument is no longer that the unbanked now have accounts, but that they now have loans. The Andhra Pradesh venue is strategically telling, as the BJP seeks to deepen its footprint in a state where it has historically played second fiddle to regional parties. If the next Budget expands credit guarantee allocations, this speech will read as the political preamble to that fiscal move.

NationPress

17 Jul 2026

Frequently Asked Questions

What did Nirmala Sitharaman say in Narasaraopeta on 17 July 2026?

She said that since 2014, PM Modi has transformed India's banking landscape with a vision of reaching every village and citizen, and that the Credit Guarantee framework has enabled first-time entrepreneurs and street vendors to access institutional credit for the first time.

What is the Credit Guarantee framework in India?

The Credit Guarantee framework refers to government-backed guarantees that allow banks to extend collateral-free loans to first-time borrowers, MSMEs, and street vendors by absorbing the risk of default on behalf of borrowers who lack personal assets to pledge.

What schemes has the Modi government launched for financial inclusion since 2014?

The three main schemes are Pradhan Mantri Jan Dhan Yojana (August 2014) for zero-balance bank accounts, MUDRA Yojana (April 2015) for micro-credit up to ₹10 lakh to small businesses, and PM SVANidhi (June 2020) for collateral-free loans to street vendors.

Why did Nirmala Sitharaman visit Narasaraopeta in Andhra Pradesh?

Narasaraopeta is a parliamentary constituency in Andhra Pradesh where Sitharaman addressed a gathering on banking outreach and financial inclusion, reflecting the BJP's continued political engagement with the state's informal-economy voters.

What is the difference between Jan Dhan and MUDRA Yojana?

Jan Dhan Yojana focuses on opening zero-balance bank accounts and providing basic insurance to unbanked households, while MUDRA Yojana goes a step further by offering micro-credit loans of up to ₹10 lakh to non-corporate small businesses and entrepreneurs.