Is the US Set to Revitalize Small and Community Banks?

Synopsis

In a pivotal move, the US government is focusing on revitalizing small and community banks to enhance local lending and stimulate economic growth. Treasury Secretary Scott Bessent emphasizes the need for tailored regulations, highlighting the importance of these institutions in supporting local economies. Can this initiative reshape the financial landscape for communities across America?

Key Takeaways

Community banks play a crucial role in local economies.

Over 50% of community banks have disappeared since the financial crisis.

Regulatory reforms are aimed at tailored regulations for small banks.

Revival of local banks can enhance housing supply .

There are concerns about potential risks of deregulation.

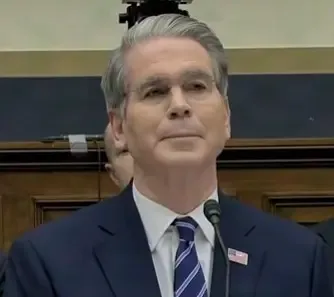

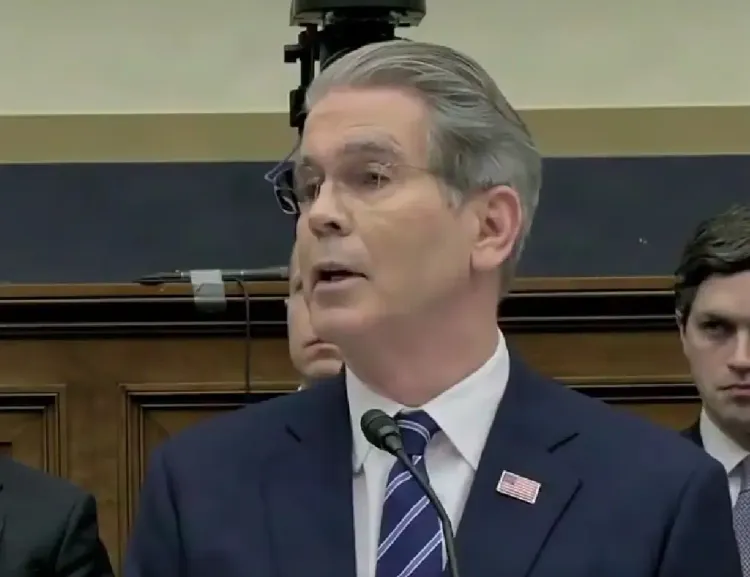

Washington, Feb 5 (NationPress) The United States is taking steps to revitalize small and community banks, asserting that years of stringent regulation have hampered local lending capabilities and hindered economic advancement, according to Treasury Secretary Scott Bessent during his testimony before Congress.

While addressing the House Financial Services Committee on Wednesday (local time), Bessent emphasized the vital role community banks play in supporting small businesses, agriculture, and housing. However, he noted their gradual disappearance since the global financial crisis.

“Over half of community banks have vanished since the onset of the great financial crisis,” Bessent remarked, highlighting that this decline has persisted even after the crisis concluded.

He attributed this trend to uniform regulations that have squeezed smaller lenders, redirecting credit towards larger institutions. Bessent pointed out that regulators often equate the risks posed by small banks with those of the nation’s largest banks.

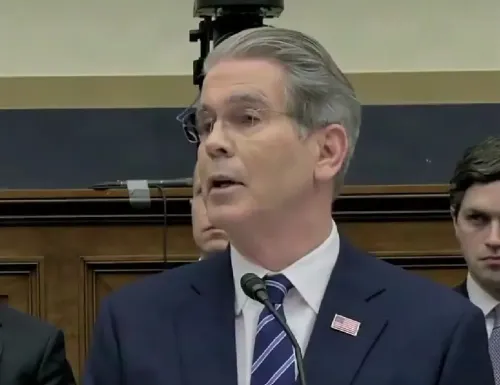

During his address to lawmakers, Bessent explained that previous regulatory frameworks imposed compliance costs on community banks, which curtailed their lending potential. He mentioned that the administration is now advocating for customized regulations that align with the size and risk profile of each institution.

Republican lawmakers supported this strategy, contending that small banks possess the best understanding of their communities and are crucial in financing local housing, farms, and small enterprises.

Bessent indicated that community banks are responsible for a significant portion of credit in agriculture, small commercial real estate, and local businesses. He cautioned that ongoing consolidation risks diminishing competition and restricting credit access beyond major financial hubs.

He asserted that revitalizing local banks would contribute to increased housing supply and stimulate economic growth outside of large metropolitan areas. “It’s time for Main Street,” Bessent conveyed to the committee.

Conversely, Democratic lawmakers expressed apprehension that relaxing regulations might elevate financial risks. They cautioned that prior deregulation had led to financial instability, underscoring the necessity for safeguards to avert a recurrence of past crises.

Bessent dismissed parallels to the pre-2008 financial collapse, asserting that excessive regulation can jeopardize stability by stifling growth and diminishing lending capacity.

He announced that the Financial Stability Oversight Council is collaborating with banking regulators to modernize oversight and alleviate unnecessary burdens, particularly for small and mid-sized banks.

The administration’s initiative also encompasses encouraging the establishment of new banks, which Bessent noted has been infrequent in recent years. Before the financial crisis, he highlighted, numerous new banks were established annually.

Bessent concluded that restoring a diversified banking system with robust community lenders would enhance the resilience of the US financial framework over time.

Point of View

It is imperative to recognize the potential benefits of revitalizing community banks. This initiative could enhance local economies by providing tailored financial solutions and increasing competition. However, it is essential to balance deregulation with necessary safeguards to ensure financial stability and prevent history from repeating itself.

NationPress

30 Jun 2026

Frequently Asked Questions

Why are community banks important?

Community banks are vital as they understand local needs and provide tailored financial services to small businesses, agriculture, and housing, driving economic growth.

What caused the decline of community banks?

The decline has primarily been due to stringent regulations that have disproportionately affected smaller lenders, pushing credit towards larger institutions.

What are tailored regulations?

Tailored regulations are customized rules designed to align with the size and risk profile of each financial institution, ensuring they are not burdened by one-size-fits-all laws.

How could revitalizing community banks impact local economies?

Revitalizing community banks could enhance access to credit, support small businesses, and promote economic growth beyond major metropolitan areas.

What concerns do lawmakers have regarding deregulation?

Lawmakers express concerns that loosening regulations could lead to increased financial risks and instability, emphasizing the need for safeguards.