Chhattisgarh Cabinet approves VAT tribunal abolition bill

Synopsis

The Chhattisgarh cabinet has approved the VAT Amendment Bill 2026 to abolish the state's Commercial Tax Tribunal, citing a sharp fall in VAT second appeals after GST and the establishment of GSTAT. Pending cases will move to the Board of Revenue for faster disposal.

Key Takeaways

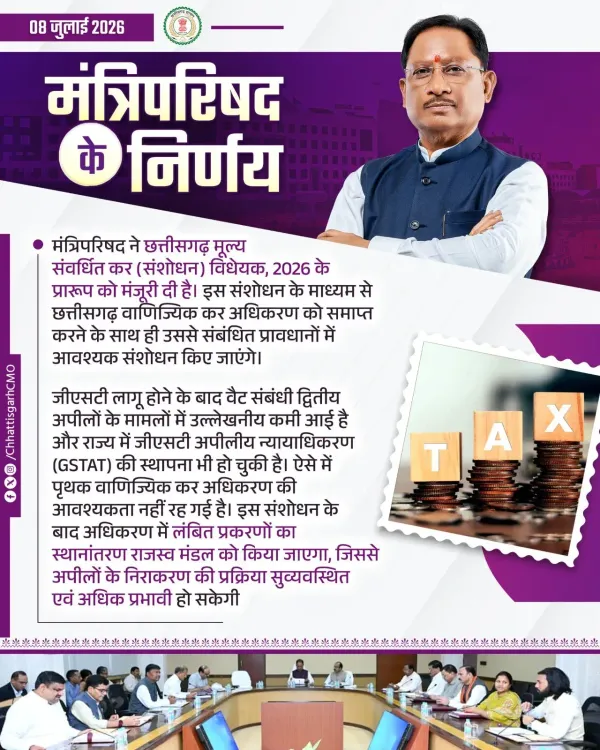

The Chhattisgarh cabinet approved the draft Chhattisgarh Value Added Tax (Amendment) Bill, 2026 on 8 July 2026 .

The bill proposes to abolish the Chhattisgarh Commercial Tax Tribunal , the state's pre-GST body for VAT second appeals.

The rationale: VAT second-appeal volumes have fallen sharply since GST was introduced on 1 July 2017 , and GSTAT is now operational in the state.

All cases pending before the tribunal will be transferred to the Board of Revenue after the amendment takes effect.

The bill must still be passed by the Chhattisgarh Legislative Assembly before becoming law.

The move is part of a broader national pattern of states winding down standalone pre-GST tax appellate bodies.

The Chief Minister's Office of Chhattisgarh announced on Wednesday, 8 July 2026 that the state cabinet has approved the draft Chhattisgarh Value Added Tax (Amendment) Bill, 2026, which proposes to abolish the Chhattisgarh Commercial Tax Tribunal and transfer its pending cases to the Board of Revenue.

Context

The cabinet's decision, shared by the Chief Minister's Office on its official X account, states in Hindi: 'मंत्रिपरिषद ने छत्तीसगढ़ मूल्य संवर्धित कर (संशोधन) विधेयक, 2026 के प्रारूप को मंजूरी दी है' ('The council of ministers has approved the draft Chhattisgarh Value Added Tax Amendment Bill, 2026'). The post further notes that second appeals related to VAT have declined significantly since the rollout of the Goods and Services Tax (GST), and that the GST Appellate Tribunal (GSTAT) has already been established in the state, making a separate commercial tax tribunal redundant.

Once the amendment is enacted, all cases pending before the Chhattisgarh Commercial Tax Tribunal will be transferred to the Board of Revenue, which the government says will make the resolution of appeals 'more streamlined and effective.'

Policy Backdrop

The Chhattisgarh Commercial Tax Tribunal was the state's pre-GST appellate body for handling second appeals in VAT and commercial tax matters. When GST was rolled out nationally on 1 July 2017, it subsumed VAT and created a unified indirect-tax appellate framework, sharply reducing the volume of new VAT second-appeal filings at state tribunals.

Across India, states have progressively rationalised such pre-GST bodies to eliminate duplication, transferring residual VAT caseloads to existing revenue or commercial-tax appellate authorities. Chhattisgarh's move follows this broader administrative-consolidation pattern, anchored by the operationalisation of GSTAT — the statutory appellate body created under the GST regime to adjudicate disputes arising from first-appellate orders in GST cases.

Stakeholders and Impact

The primary stakeholders are VAT appellants — businesses and traders who had filed or may file second appeals under the older VAT regime — and the state tax department. For appellants, the transfer to the Board of Revenue means their cases will be heard by an established, multi-jurisdictional authority rather than a single-purpose tribunal whose docket has thinned considerably since 2017.

For the state government, abolishing the tribunal eliminates the administrative and financial overhead of maintaining a dedicated body for a declining category of disputes. The Board of Revenue, as Chhattisgarh's apex revenue appellate authority, already handles land, excise and certain tax-related appeals, making it a natural repository for residual VAT cases.

What's Next

The draft bill must now be introduced and passed in the Chhattisgarh Legislative Assembly before it can be notified as law. Following enactment, the government will need to frame and notify rules governing the transfer of pending cases to the Board of Revenue and set timelines for their disposal. The smooth migration of the pending caseload will be the key operational test of the reform's stated goal of a more effective appeals process.

If the bill clears the Assembly without significant amendment, Chhattisgarh will join the growing list of Indian states that have formally wound down their standalone VAT appellate tribunals — a structural shift that signals the near-complete institutional transition from the pre-GST indirect-tax architecture to the unified GST framework.

Point of View

The state avoids the cost of maintaining a near-idle quasi-judicial body while leveraging an institution with established capacity. The move also signals Chhattisgarh's alignment with the national consensus on post-GST institutional clean-up, which several other states completed earlier. The real governance test, however, will come in the Assembly and in the framing of transfer rules — delays there could leave VAT appellants in procedural limbo.

NationPress

8 Jul 2026

Frequently Asked Questions

What is the Chhattisgarh VAT Amendment Bill 2026?

The Chhattisgarh Value Added Tax (Amendment) Bill, 2026 is a draft legislation approved by the state cabinet on 8 July 2026 that proposes to abolish the Chhattisgarh Commercial Tax Tribunal and transfer its pending cases to the Board of Revenue.

Why is Chhattisgarh abolishing the Commercial Tax Tribunal?

The government says VAT-related second appeals have declined significantly since GST was introduced in 2017, and the GST Appellate Tribunal (GSTAT) is now operational in the state, making a separate commercial tax tribunal unnecessary.

What will happen to pending VAT cases in Chhattisgarh?

Once the amendment bill is enacted, all cases pending before the Commercial Tax Tribunal will be transferred to the Board of Revenue, Chhattisgarh's apex revenue appellate authority.

What is GSTAT and does Chhattisgarh have one?

GSTAT, the GST Appellate Tribunal, is the statutory appellate body under the GST regime for disputes arising from first-appellate orders in GST cases. According to the cabinet's announcement, GSTAT has already been established in Chhattisgarh.

Has the Chhattisgarh VAT Amendment Bill 2026 become law yet?

No. As of 8 July 2026, the cabinet has only approved the draft bill. It must be introduced and passed by the Chhattisgarh Legislative Assembly before it becomes law.