India's nuclear sector eyes $210 billion opportunity after SHANTI Act

Synopsis

A new YCP white paper puts a $210 billion figure on India's nuclear opportunity — and the SHANTI Act is the unlock. With a 100 GW target by 2047 against a 9 GW base today, the gap is enormous. Private capital is now legally welcome for the first time, but financing depth, liability clarity, and regulatory speed will decide whether this becomes India's biggest clean-energy build-out or another ambitious number that stalls at the policy stage.

Key Takeaways

India targets 100 GW of nuclear capacity by 2047 , up from a current base of 9 GW — a more than 10-fold expansion.

The required capital outlay is estimated at $210 billion , according to a YCP white paper.

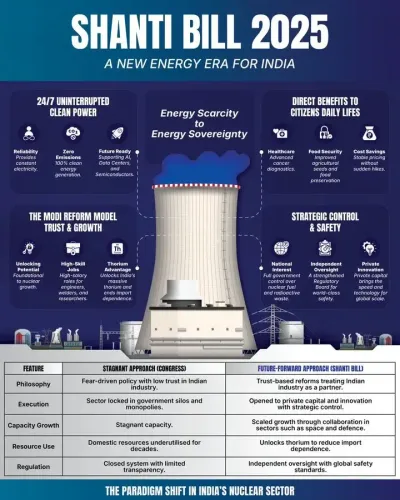

The SHANTI Act (2025) allows private companies to own and operate nuclear power assets for the first time, while the government retains control over fuel cycles, enrichment, and waste management.

The opportunity spans generation, industrial applications, component manufacturing, and advanced reactor development across the full value chain.

Key gaps identified include financing depth, execution capacity, and residual policy ambiguity around liability frameworks.

Global models from the United States and Canada are cited as reference points for structuring private participation.

India's nuclear industry is on the cusp of a structural transformation, shifting from a decades-old state-controlled model to a commercially open ecosystem — and the price tag on that opportunity is an estimated $210 billion, according to a new white paper released by consultancy firm YCP.

The Scale of the Opportunity

The white paper, titled 'Unlocking India's Nuclear Sector: Commercial Opportunities Created by the SHANTI Act', notes that India has set a target of 100 GW of nuclear capacity by 2047 — more than 10 times its current installed base of 9 GW. Reaching that target will require capital and execution capacity that the public sector alone cannot supply, the report states.

The opportunity spans the entire value chain: large-scale grid-connected plants, captive industrial reactors, engineering and construction, component manufacturing, and advanced reactor development. Nuclear is positioned in the report as a critical backbone of India's energy transition, supporting both grid stability and industrial decarbonisation.

What the SHANTI Act Changes

The SHANTI Act (2025) marks the legislative turning point. The law opens nuclear power generation to private ownership and operation for the first time, while retaining government control over strategically sensitive areas — fuel cycles, enrichment, and waste management. The report describes this as a major step in India's nuclear sector privatisation, ending a model that was intentionally centralised since independence.

For decades, that centralised approach built a strong technical foundation, but it was not designed for rapid scale-up. The reform attempts to correct that constraint by broadening the pool of eligible investors and operators.

Global Lessons and Remaining Gaps

Drawing on international case studies, the white paper outlines the conditions that have enabled private participation elsewhere — revenue stability, clear liability frameworks, and robust regulatory oversight. It specifically examines the United States' private-ownership model and Canada's nuclear concession model as reference points for India's policymakers.

The report also identifies gaps that could slow the sector's scale-up: financing depth, execution capacity, and residual policy ambiguity. These, it argues, will determine how quickly a viable investment ecosystem takes shape.

What Industry Voices Are Saying

Ankit Hoshing, Partner at YCP India, said: 'India's nuclear sector is moving from a strategic programme to a commercial platform. The opportunity is clear, but its pace will depend on how quickly a viable investment ecosystem takes shape.'

What Comes Next

With the SHANTI Act now on the books, the focus shifts to implementation — sectoral guidelines, liability norms, and financing structures that can attract domestic and foreign private capital at the scale the 100 GW by 2047 target demands. Industry observers note that the window is open, but the clock is running.

Point of View

But the harder question is whether India's regulatory and financing infrastructure can absorb private capital at that scale. The SHANTI Act is a necessary condition, not a sufficient one — liability frameworks remain underspecified, and no domestic financing vehicle of the required depth yet exists. India has a history of bold energy targets that outpace execution: solar hit its numbers, but only after years of policy iteration and tariff pain. Nuclear is an order of magnitude more complex. The real test of the SHANTI Act will come in the first private project financial close, not in the white paper.

NationPress

29 Jun 2026

Frequently Asked Questions

What is the $210 billion nuclear investment opportunity in India?

It refers to the estimated capital required for India to expand its nuclear power capacity from 9 GW today to 100 GW by 2047 , as outlined in a white paper by consultancy firm YCP. The opportunity spans power generation, industrial reactors, component manufacturing, and advanced reactor development.

What is the SHANTI Act and why does it matter?

The SHANTI Act (2025) is a landmark Indian legislation that opens nuclear power generation to private ownership and operation for the first time. It allows companies to own and run nuclear assets while the government retains control over sensitive areas such as fuel cycles, enrichment, and waste management — marking a fundamental shift from India's historically state-led nuclear model.

What is India's nuclear capacity target for 2047?

India has set a target of 100 GW of nuclear capacity by 2047, compared to its current installed base of approximately 9 GW. Achieving this requires more than a 10-fold expansion and an estimated $210 billion in capital investment.

What gaps could slow India's nuclear sector growth?

The YCP white paper identifies three key gaps: financing depth, execution capacity, and policy clarity — particularly around liability frameworks. Without these, private capital is unlikely to commit at the scale the 100 GW target demands.

Which global nuclear models is India looking at for reference?

The white paper examines the United States' private-ownership model and Canada's nuclear concession model as international benchmarks for structuring private participation in India's nuclear sector.