SIDBI must become MSME growth partner, not just lender: FM Sitharaman

Synopsis

Finance Minister Nirmala Sitharaman’s message to SIDBI in Mumbai was blunt: stop treating a resort, a farmer-linked enterprise, and an auto-parts supplier as the same borrower. Her call to redesign lending around business cycles — and to build out venture debt for startups — reframes SIDBI’s identity from a development lender into an active risk-sharing partner for India’s 11-crore-employing MSME sector.

Key Takeaways

Finance Minister Nirmala Sitharaman addressed an event in Mumbai on 25 May 2025 , urging SIDBI to evolve beyond a lending role.

She called for credit products designed around each enterprise’s business cycle — rejecting a one-size-fits-all repayment model.

Sitharaman asked SIDBI to become a market maker and risk-sharing partner for India’s MSME and startup ecosystem.

She also directed SIDBI to deepen the venture capital debt market so startups can access patient, flexible capital.

The minister said improving SIDBI’s capital base will allow it to raise lower-cost funds and pass the benefit on to small entrepreneurs.

Union Finance Minister Nirmala Sitharaman on Monday, 25 May called on the Small Industries Development Bank of India (SIDBI) to move beyond its conventional lending role and transform into a market maker and risk-sharing partner for India's MSME and startup ecosystem. Addressing an event in Mumbai, the minister argued that standard financial products are fundamentally ill-suited to the non-standard business realities of small enterprises.

The Core Argument: One Size Does Not Fit All

Sitharaman made a pointed case for sector-sensitive credit design, drawing on the uneven cash flows that define many MSME segments. “A farmer-linked enterprise does not earn every month, a resort does not earn evenly through the year, a government exporter waits for payment after shipment, and a small auto component supplier waits for invoice clearance. Then why should all of them be given the same repayment structure?” she said.

The minister stressed that credit products must be structured around each enterprise’s business cycle rather than applying a uniform repayment template. Enterprises tied to farming, tourism, exports, and manufacturing face inherently seasonal or delayed revenue patterns, yet are routinely subjected to identical loan structures by banks and financial institutions — a mismatch she described as a structural problem requiring deliberate redesign.

What the Minister Expects from SIDBI

“SIDBI’s role must now expand from being only a lender to becoming a market maker and risk-sharing partner for India’s MSME and startup ecosystem,” Sitharaman stated. She also called on the institution to deepen the venture capital debt market for startups, ensuring that innovative enterprises can access “patient, flexible and growth-oriented capital.”

The minister further indicated that SIDBI’s capital base is being strengthened specifically to enable it to raise lower-cost funds — savings that should, in her view, be passed on to small entrepreneurs through wider, cheaper, and more accessible credit. “By improving SIDBI’s capital, we are ensuring that the institution can raise lower-cost funds and pass that benefit on to small entrepreneurs through wider, cheaper and more accessible credit,” she said.

Why This Matters for India’s MSME Sector

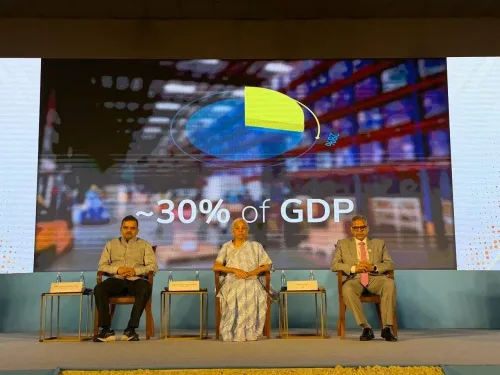

India’s MSME sector employs an estimated 11 crore people and contributes roughly 30% of GDP, yet access to formal, affordable credit remains a persistent bottleneck. The call to redesign SIDBI’s mandate comes at a time when the Centre has been ramping up policy attention on small businesses — from the revised MSME classification thresholds to the Udyam registration push. Notably, this is not the first time the government has flagged the rigidity of bank lending norms as a drag on MSME growth; the Reserve Bank of India (RBI) has also periodically nudged lenders toward more flexible credit frameworks for small enterprises.

Venture Capital Debt and the Startup Angle

Sitharaman’s call to deepen the venture capital debt market signals a broader ambition: positioning SIDBI as a bridge between traditional development finance and the risk capital that early-stage businesses need. Venture debt — loans structured for high-growth startups that may not yet be profitable — remains underdeveloped in India relative to markets like the United States and the United Kingdom. A more active SIDBI in this space could reduce the dependence of Indian startups on equity dilution at early stages.

What Comes Next

No specific timeline or outlay was announced at the event. Industry bodies representing MSMEs and startup founders are expected to engage with SIDBI on operationalising the minister’s directions. The degree to which SIDBI can institutionalise flexible lending will depend on regulatory headroom from the RBI and the institution’s own capacity to assess non-standard credit risk. Observers will watch whether these directions translate into revised product guidelines in the near term.

Point of View

And SIDBI is the logical candidate. But without a regulatory framework that lets it absorb higher credit risk, the ambition will stay rhetorical. The minister’s credibility here will be measured by whether revised product guidelines follow within a defined timeframe.

NationPress

14 Jul 2026

Frequently Asked Questions

What did Finance Minister Nirmala Sitharaman say about SIDBI?

Sitharaman called on SIDBI to move beyond its traditional lending role and become a market maker and risk-sharing partner for India’s MSME and startup ecosystem. She made the remarks at an event in Mumbai on 25 May 2025, urging the institution to design credit products around the unique business cycles of small enterprises rather than applying uniform repayment structures.

Why does Sitharaman want SIDBI to change its lending model?

The minister argued that businesses linked to farming, tourism, exports, and manufacturing have uneven or delayed revenue cycles, yet are subjected to the same repayment structures as any other borrower. She said standard financial products cannot serve non-standard businesses, and that SIDBI must redesign lending to reflect these realities.

What is venture capital debt, and why is SIDBI being asked to deepen it?

Venture capital debt refers to loans structured for high-growth startups that may not yet be profitable, offering an alternative to equity dilution. Sitharaman asked SIDBI to expand this market so innovative enterprises can access patient, flexible, and growth-oriented capital — an area that remains underdeveloped in India compared to more mature startup markets.

How will improving SIDBI’s capital base help small businesses?

According to Sitharaman, a stronger capital base will allow SIDBI to raise funds at lower cost and pass those savings on to small entrepreneurs through wider, cheaper, and more accessible credit. The government has been working to bolster SIDBI’s finances specifically for this purpose.

What happens next after the Finance Minister’s directions to SIDBI?

No specific timeline or financial outlay was announced at the Mumbai event. Industry bodies and startup representatives are expected to engage with SIDBI on implementation. Observers will watch for revised product guidelines and any regulatory changes from the RBI that would give SIDBI the headroom to take on non-standard credit risk.